Can you get a home equity loan on a vacation home

Nathan Sanders

Published Mar 01, 2026

You don’t have to sell your vacation home to access the equity it’s built up. Instead, you could access the value of your home using a cash–out refinance, home equity loan, or home equity line of credit (HELOC). … Fortunately, many lenders and banks are offering home equity loans on second homes.

Can I get a home equity loan on my vacation home?

You don’t have to sell your vacation home to access the equity it’s built up. Instead, you could access the value of your home using a cash–out refinance, home equity loan, or home equity line of credit (HELOC). … Fortunately, many lenders and banks are offering home equity loans on second homes.

Does Heloc have to be on primary residence?

A Home Equity Line of Credit can be used on primary residences, second homes and investment properties.

Can you use home equity for down payment on second home?

You can take out a home equity loan (HEL) or home equity line of credit (HELOC) to make the down payment on your second home. Your first home serves as collateral. Advantages of HELs and HELOCs as a down payment include the following: … You may be able to deduct the interest paid on home equity debt, up to $100,000.How much equity do you need to buy a second house?

Equity is the difference between your property value and the amount you have owing on your home loan. To qualify: You can generally release up to 80-90% of the value in your property in equity to buy a second property. You must owe less than 80% of the property value on your home loan.

How can I get approved for 2 mortgages?

To be approved for a second mortgage, you’ll likely need a credit score of at least 620, though individual lender requirements may be higher. Plus, remember that higher scores correlate with better rates. You’ll also probably need to have a debt-to-income ratio (DTI) that’s lower than 43%.

How do you finance a second home?

- Home Equity Financing. Home equity products are one of the most popular ways to finance a second home because they allow access to large amounts of cash at relatively low interest rates. …

- Reverse Mortgage. …

- Cash-Out Refinance. …

- Loan Assumption. …

- 401(k) Loan.

What are the disadvantages of a home equity line of credit?

- HELOCs can come with a minimum withdrawal amount.

- There can be limitations to how you access the funds.

- There is a set withdraw period after which you cannot access any further funds.

- There can be fees associated with a HELOC.

- You can hurt your credit if you do not make payments on time.

- Harder to qualify right now.

How can I get rid of my mortgage to buy another house?

- Sell Your House. One of the best and fastest ways to get out of a mortgage is to sell the property and use the proceeds to pay off the loan. …

- Turn Over Ownership to Your Lender. …

- Let the Lender Seek Foreclosure. …

- Seek a Short Sale. …

- Rent Out Your Home. …

- Ask for a Loan Modification. …

- Just Walk Away.

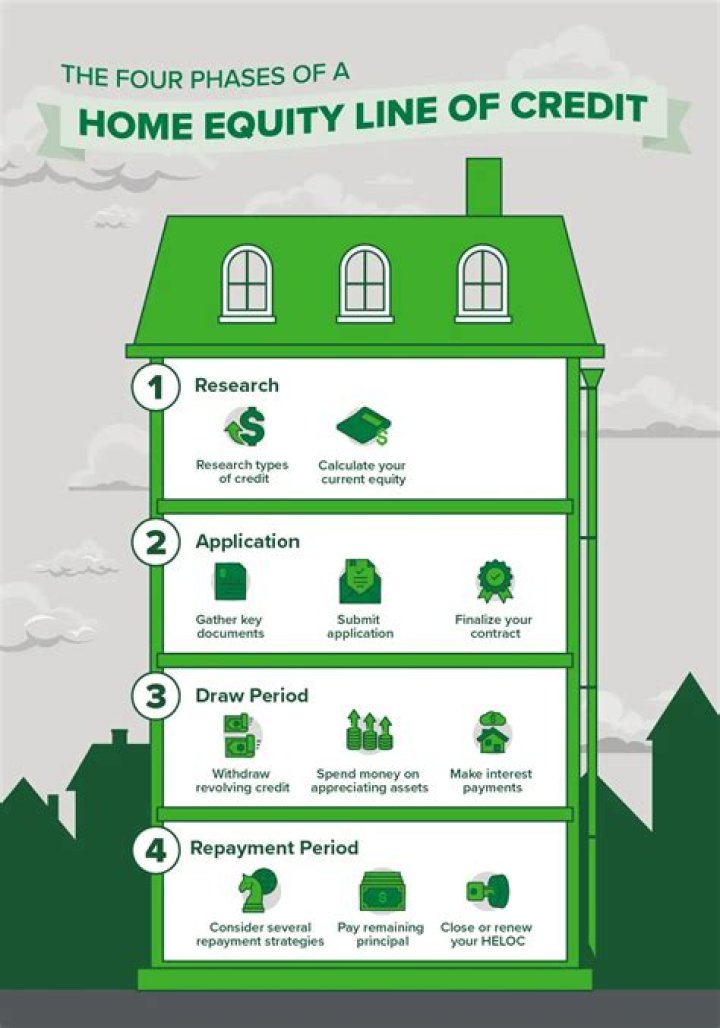

How long does it take to get the money? It can take up to four weeks to close on a HELOC. Of course, several factors can impact that timeline, such as the appraisal process and documentation delays. You may have to wait a few days, or even weeks, to access your funds after closing.

Article first time published onHow much equity can you take out on a home equity loan?

Depending on your financial history, lenders generally want to see an LTV of 80% or less, which means your home equity is 20% or more. In most cases, you can borrow up to 80% of your home’s value in total. So you may need more than 20% equity to take advantage of a home equity loan.

Is having 2 mortgages a good idea?

Advantages of second mortgages include higher loan amounts, lower interest rates, and potential tax benefits. Disadvantages of second mortgages include the risk of foreclosure, loan costs, and interest costs. Second mortgages are often used for items such as home improvement or debt consolidation.

Do I need a deposit if I have equity?

A popular way to buy an investment property is to use the equity in your existing home, meaning you don’t have to put any physical cash towards the deposit.

Can I buy a second home with a current mortgage?

You can use the equity in your current home to buy a second home by taking out either a home equity loan or a cash-out refinance. The money that you receive from this loan or refinance can then be put towards the down payment on your second home.

Can you have two primary residences?

The short answer is that you cannot have two primary residences. You will need to figure out which of your homes will be considered your primary residence and file your taxes accordingly.

Are mortgage rates higher for 2nd homes?

Mortgage rates are higher for second homes and investment properties than for the home you live in. Generally, investment property rates are about 0.5% to 0.75% higher than market rates. For a second home or vacation home, they’re only slightly higher than the rate you’d qualify for on a primary residence.

What is the minimum down payment for a second home?

To qualify for a loan on a second home, you’ll need a down payment of at least 10%. Keep in mind that restrictions on what is and isn’t considered a second home may apply. For example, you can only rent the home for up to 180 days a year. FHA Loan: You cannot use an FHA loan to buy a second property.

What is a piggyback loan?

A “piggyback” second mortgage is a home equity loan or home equity line of credit (HELOC) that is made at the same time as your main mortgage. Its purpose is to allow borrowers with low down payment savings to borrow additional money in order to qualify for a main mortgage without paying for private mortgage insurance.

How much can I borrow if I already have a mortgage?

How much can I borrow if I already have a mortgage? Most mortgage lenders will let you borrow up to 4.5 times your salary, but the size of the second mortgage you qualify for is also determined by the amount of equity you have, along with your credit history.

Can I buy another house if I already have one?

Bear in mind that you may need a large down payment in order to qualify for a second home mortgage. Some lenders ask for a down payment of 20 percent but others can go as high as 32 percent, depending on the property. The pre-approval should state the maximum purchase price and loan amount for the new home.

How long does home equity loan process take?

The truth is that home equity loan approval can take anywhere from a week—or two up to months in some cases. Most lenders will tell you that the average window of time it takes to get a home equity loan is between two and six weeks, with most closings happening within a month.

What does a bridge loan cost?

Bridge loan interest rates typically range between 6% to 10%. Meanwhile, traditional commercial loan rates range from 1.176% to 12%. Borrowers can secure a lower interest rate with a traditional commercial loan, especially with a high credit score.

How do I know how much equity I have in my home?

You can figure out how much equity you have in your home by subtracting the amount you owe on all loans secured by your house from its appraised value. This includes your primary mortgage as well as any home equity loans or unpaid balances on home equity lines of credit.

What scenario do most homeowners use the equity in their home?

Homeowners sometimes use home equity to pay off other personal debts, such as car loans or credit cards. “This is another very popular use of home equity, as one is often able to consolidate debt at a much lower rate over a longer-term and reduce their monthly expenses significantly,” Hackett says.

Are home equity loans tax deductible?

Interest on a home equity line of credit (HELOC) or a home equity loan is tax deductible if you use the funds for renovations to your home—the phrase is “buy, build, or substantially improve.” To be deductible, the money must be spent on the property in which the equity is the source of the loan.

What percentage of home value can you get a home equity loan?

A home equity loan generally allows you to borrow around 80% to 85% of your home’s value, minus what you owe on your mortgage. You can do some simple math to estimate how much you might be able to borrow.

What is the monthly payment on a $200 000 home equity loan?

On a $200,000, 30-year mortgage with a 4% fixed interest rate, your monthly payment would come out to $954.83 — not including taxes or insurance.

Can you use equity to pay closing costs?

Home equity loan closing costs can range from 2% to 5% of your loan amount. A home equity loan allows you to borrow a lump sum against your available equity, and can help you cover home improvements, pay college costs or consolidate high-interest debt.

How much equity can I get in my home after 5 years?

In the first year, nearly three-quarters of your monthly $1000 mortgage payment (plus taxes and insurance) will go toward interest payments on the loan. With that loan, after five years you’ll have paid the balance down to about $182,000 – or $18,000 in equity.

What is the monthly payment on a $100 000 home equity loan?

Assuming principal and interest only, the monthly payment on a $100,000 loan with an APR of 3% would come out to $421.60 on a 30-year term and $690.58 on a 15-year one. Credible is here to help with your pre-approval.

What is the payment on a 50000 home equity loan?

Loan payment example: on a $50,000 loan for 120 months at 3.80% interest rate, monthly payments would be $501.49.