Do you pay capital gains if you sell at a loss

Sarah Rodriguez

Published May 02, 2026

If you sell something for less than its basis, you have a capital loss. … If you have $50,000 in long-term gains from the sale of one stock, but $20,000 in long-term losses from the sale of another, then you may only be taxed on $30,000 worth of long-term capital gains.

Do you pay capital gains on losses?

Yes, but there are limits. Losses on your investments are first used to offset capital gains of the same type. So, short-term losses are first deducted against short-term gains, and long-term losses are deducted against long-term gains.

What happens if you take a loss on selling your house?

If you sell your primary residence at a loss, you won’t be able to deduct that loss on your tax return. If the sale price is higher than the purchase price, the IRS will consider that a gain, and you’ll need to pay taxes on it, even if you have outstanding mortgage balances that are higher than the sale price.

Do you pay capital gains if you sell your house at a loss?

If you sell the capital asset for more than you paid for it and earn a profit, you are subject to tax on the gain. If you end up selling for less than your cost, you incur a loss. … However, losses on personal-use assets are generally not deductible.How much capital gains loss can I claim?

Your maximum net capital loss in any tax year is $3,000. The IRS limits your net loss to $3,000 (for individuals and married filing jointly) or $1,500 (for married filing separately). Any unused capital losses are rolled over to future years. If you exceed the $3,000 threshold for a given year, don’t worry.

Do seniors pay capital gains tax?

Today, anyone over the age of 55 does have to pay capital gains taxes on their home and other property sales. There are no remaining age-related capital gains exemptions. However, there are other capital gains exemptions that those over the age of 55 may qualify for.

Can business loss offset capital gain?

Long-term capital loss will only be adjusted towards long-term capital gains. However, a short-term capital loss can be set off against both long-term capital gains and short-term capital gain. … But the losses from any other businesses or profession can be set off against profits from the specified businesses.

Do I pay tax when I sell my house Australia?

Generally, you don’t pay capital gains tax (CGT) if you sell the home you live in (under the main residence exemption). … Some states charge stamp duty when you buy a property, including a home. Some states also levy land tax on land that exceeds a certain value, though the property you live in is usually exempt.How do I avoid capital gains on sale of property?

However, to avoid tax on short-term capital gains, the only way out is to set it off against any short-term loss from the sale of other assets such as stocks, gold or another property. To plug tax leaks, the government has now made it mandatory for buyers to deduct TDS when they buy a house worth over Rs 50 lakh.

Can you take a capital loss on sale of second home?A second home, or a timeshare, used as a vacation home is a personal use capital asset. A gain on the sale is reportable income, but a loss is NOT deductible. You may receive IRS Form 1099-S Proceeds from Real Estate Transactions for the sale of your vacation home.

Article first time published onCan you claim a loss on sale of property?

Losses from selling a personal residence are not deductible. Generally, you can only claim tax losses for sales of property used for business or investment purposes. … However, a loss from a decline in value after conversion to a rental, is generally a deductible loss.

Is tax loss harvesting worth it?

The Bottom Line It’s generally a poor decision to sell an investment, even one with a loss, solely for tax reasons. Nevertheless, tax-loss harvesting can be a useful part of your overall financial planning and investment strategy, and should be one tactic toward achieving your financial goals.

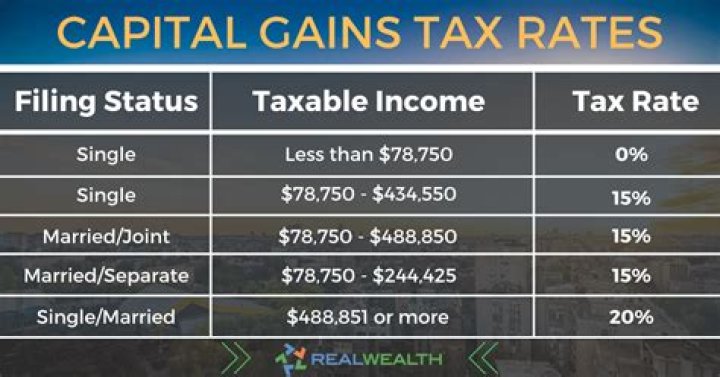

What is the capital gain tax for 2020?

Capital Gains Tax RateTaxable Income (Single)Taxable Income (Married Filing Separate)0%Up to $40,000Up to $40,00015%$40,001 to $441,450$40,001 to $248,30020%Over $441,450Over $248,300

Do you have to report capital losses?

Capital assets held for personal use that are sold at a loss generally do not need to be reported on your taxes. The loss is generally not deductible, as well. The gains you report are subject to income tax, but the rate of tax you’ll pay depends on how long you hold the asset before selling.

How long can you run a business at a loss?

Tip. In a five-year period, you can claim a business net loss up to two years without any tax problems. If you report operating losses more frequently, the Internal Revenue Service (IRS) might rule your business is only a hobby. In that case, you’d have to report the income but couldn’t write off any expenses.

Can you offset capital gains with ordinary losses?

An ordinary loss will offset ordinary income and capital gains on a one-to-one basis. A capital loss is strictly limited to offsetting a capital gain and up to $3,000 of ordinary income. The remaining capital loss must be carried over to another year. … Net your long-term capital gains and losses.

Can long term capital loss offset short term capital gain?

Set off of Capital Losses Long Term Capital Loss can be set off only against Long Term Capital Gains. Short Term Capital Losses are allowed to be set off against both Long Term Gains and Short Term Gains.

How do I avoid capital gains tax when I retire?

- Hold onto taxable assets for the long term. …

- Make investments within tax-deferred retirement plans. …

- Utilize tax-loss harvesting. …

- Donate appreciated investments to charity.

What is the capital gains exemption for 2021?

Married investors filing jointly with taxable income of $80,800 or less ($40,400 for single filers) may pay 0% long-term capital gains levies for 2021.

What is the capital gains tax rate for 2021?

For example, in 2021, individual filers won’t pay any capital gains tax if their total taxable income is $40,400 or below. However, they’ll pay 15 percent on capital gains if their income is $40,401 to $445,850. Above that income level, the rate jumps to 20 percent.

How long do you have to keep a property to avoid capital gains tax?

Live in the house for at least two years. The two years don’t need to be consecutive, but house-flippers should beware. If you sell a house that you didn’t live in for at least two years, the gains can be taxable.

How long do you have to live in a property to avoid capital gains tax?

To get around the capital gains tax, you need to live in your primary residence at least two of the five years before you sell it. Note that this does not mean you have to own the property for a minimum of 5 years, however. Once you’ve lived in the property for at least 2 years, you’d reach capital gains tax exemption.

How do I calculate capital gains on sale of property?

In case of short-term capital gain, capital gain = final sale price – (the cost of acquisition + house improvement cost + transfer cost). In case of long-term capital gain, capital gain = final sale price – (transfer cost + indexed acquisition cost + indexed house improvement cost).

How can I avoid capital gains tax when selling a second home?

There are various ways to avoid capital gains taxes on a second home, including renting it out, performing a 1031 exchange, using it as your primary residence, and depreciating your property.

How do you report a loss on the sale of a second home?

Answer: Your second residence (such as a vacation home) is considered a capital asset. Use Schedule D (Form 1040), Capital Gains and Losses and Form 8949, Sales and Other Dispositions of Capital Assets to report sales, exchanges, and other dispositions of capital assets.

How does selling a second home affect taxes?

If you sell property that is not your main home (including a second home) that you’ve held for at least a year, you must pay tax on any profit at the capital gains rate of up to 15 percent. … Profit from selling buildings held less than a year is taxed at your regular rate.

How does selling a house at a loss affect taxes?

If you sell your home at a loss, can you deduct the amount from your taxes? Unfortunately, the answer is no. A loss on the sale of a personal residence is considered a nondeductible personal expense. You can only deduct losses on the sale of property used for business or investment purposes.

Should I sell my investment property at a loss?

In general, if you’re set to make a profit upon selling, it’s wise to wait to sell an investment property until after at least 12 months of ownership. This way, you can cut your capital gains tax charge in half.

What are capital losses?

A capital loss occurs when you sell a security or investment for less than the original purchase price or its adjusted basis. Taxpayers can use capital losses on their taxes to offset their capital gains.

At what income do you pay capital gains tax?

Capital Gain Tax Rates A capital gain rate of 15% applies if your taxable income is $80,000 or more but less than $441,450 for single; $496,600 for married filing jointly or qualifying widow(er); $469,050 for head of household, or $248,300 for married filing separately.

What happens if you don't report capital losses?

Any capital asset sales create a taxable event. You must report all sales and determine gain or loss. … If you do not report it, then you can expect to get a notice from the IRS declaring the entire proceeds to be a short term gain and including a bill for taxes, penalties, and interest.