How do you calculate portfolio variance

Ava Hall

Published Mar 30, 2026

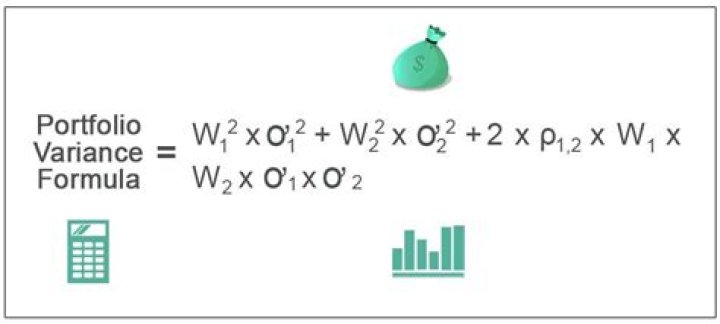

To calculate the portfolio variance of securities in a portfolio, multiply the squared weight of each security by the corresponding variance of the security and add two multiplied by the weighted average of the securities multiplied by the covariance between the securities.

How do you calculate portfolio variance in Excel?

- Variance= (20%^2*2.3%^2)+(35%^2*3.5%^2)+(45%^2*4%^2)+(2*(20%*35%*2.3%*3.5*0.6))+(2*(20%*45%*2.3%*4%*0.8))+(2*(35%*45%*3.5%*4%*0.5))

- Variance = 0.000916.

How do you calculate portfolio deviation?

- Find the Standard Deviation of each asset in the portfolio.

- Find the weight of each asset in the overall portfolio.

- Find the correlation between the assets in the portfolio (in the above case between the two assets in the portfolio).

How do you find the variance of a portfolio with 3 assets?

- Calculate the arithmetic mean (i.e. average) of the asset returns.

- Find out difference between each return value from the mean and square it.

- Sum all the squared deviations and divided it by total number of observations.

What is the formula for determining portfolio returns?

The simplest way to calculate a basic return is called the holding period return. Here’s the formula to calculate the holding period return: HPR = Income + (End of Period Value – Initial Value) ÷ Initial Value.

How do you find the variance of a stock return?

Let’s start with a translation in English: The variance of historical returns is equal to the sum of squared deviations of returns from the average ( R ) divided by the number of observations ( n ) minus 1.

How do you get the variance?

- Find the mean of the data set. Add all data values and divide by the sample size n. …

- Find the squared difference from the mean for each data value. Subtract the mean from each data value and square the result. …

- Find the sum of all the squared differences. …

- Calculate the variance.

How do you find the variance of a portfolio matrix?

- The covariance matrix is used to calculate the standard deviation of a portfolio of stocks which in turn is used by portfolio managers to quantify the risk associated with a particular portfolio.

- Expected portfolio variance= SQRT (WT * (Covariance Matrix) * W)

How do you calculate volatility of a portfolio in Excel?

Volatility is inherently related to standard deviation, or the degree to which prices differ from their mean. In cell C13, enter the formula “=STDEV. S(C3:C12)” to compute the standard deviation for the period.

How do you calculate volatility of a portfolio?Volatility for a portfolio may be calculated using the statistical formula for the variance of the sum of two or more random variables which is then square rooted. Alternatively, the volatility for a portfolio may be calculated based on the weighted average return series calculated for the portfolio.

Article first time published onWhat is portfolio variance?

Portfolio variance is a measure of the dispersion of returns of a portfolio. It is the aggregate of the actual returns of a given portfolio over a set period of time. Portfolio variance is calculated using the standard deviation of each security in the portfolio and the correlation between securities in the portfolio.

What is the portfolio standard deviation?

Definition: The portfolio standard deviation is the financial measure of investment risk and consistency in investment earnings. In other words, it measures the income variations in investments and the consistency of their returns.

How do you calculate portfolio correlation?

The formula for correlation is equal to Covariance of return of asset 1 and Covariance of return of asset 2 / Standard. Deviation of asset 1 and a Standard Deviation of asset 2.

How do I make a portfolio in Python?

- Build a portfolio around your interests. …

- Pick projects that others will understand. …

- Avoid common datasets. …

- Balance your portfolio with different projects. …

- Participate in competitions. …

- Check out portfolios of other successful data scientists. …

- Consider using Jupyter Notebook. …

- Post your code on GitHub.

How does Python calculate portfolio volatility?

- # create the correlation matrix. corr_matrix = np.corrcoef(daily_returns)

- # portfolio weights. w = np.array([ 0.3 , 0.5 , 0.2 ])

- # portfolio volatility. portfolio_volatility = np.sqrt(w.T.dot(corr_matrix).dot(w))

How do you calculate annual portfolio return?

Annualized returns are calculated to represent what an investor would earn if the returns were compounded. To calculate the annual return, divide the total returns by the number of years in the holding period. For example, if an investment has yielded 10% over a five year period, the annualized return would be 2%.

What is minimum variance portfolio?

A minimum variance portfolio is a collection of securities that combine to minimize the price volatility of the overall portfolio. Volatility is a measure of a security’s price movement (ups and downs).

What is variance and how is it calculated?

In statistics, variance measures variability from the average or mean. It is calculated by taking the differences between each number in the data set and the mean, then squaring the differences to make them positive, and finally dividing the sum of the squares by the number of values in the data set.

How do you calculate variance and standard deviation?

To calculate the variance, you first subtract the mean from each number and then square the results to find the squared differences. You then find the average of those squared differences. The result is the variance. The standard deviation is a measure of how spread out the numbers in a distribution are.

How do I find the sample variance?

- Find the mean of the data.

- Subtract the mean from each data point.

- Take the summation of the squares of values obtained in the previous step.

- Divide this value by n – 1.

What is stock variance?

The variance of stock returns is a measure of how much a stock’s return varies with respect to its average daily returns.

How do you calculate annual variance?

To calculate year-over-year variance,simply subtract the new period data from the old, then divide your result by the old data to get a variance percentage.

How do you calculate portfolio beta?

You can determine the beta of your portfolio by multiplying the percentage of the portfolio of each individual stock by the stock’s beta and then adding the sum of the stocks’ betas.

What is portfolio volatility?

Portfolio volatility is a measure of portfolio risk, meaning a portfolio’s tendency to deviate from its mean return. Remember that a portfolio is made up of individual positions, each with their own volatility measures. These individual variations, when combined, create a single measure of portfolio volatility.

Can portfolio variance negative?

Should I just assume it’s zero? A negative variance is troublesome because one cannot take the square root (to estimate standard deviation) of a negative number without resorting to imaginary numbers.

How do you calculate the variance of an n asset portfolio?

Portfolio variance is calculated by multiplying the squared weight of each security by its corresponding variance and adding twice the weighted average weight multiplied by the covariance of all individual security pairs.

How do you calculate portfolio covariance?

The covariance of two assets is calculated by a formula. The first step of the formula determines the average daily return for each individual asset. Then, the difference between daily return minus the average daily return is calculated for each asset, and these numbers are multiplied by each other.

What is the standard deviation of a fully diversified portfolio?

a. From the text, we know that the standard deviation of a well-diversified portfolio of common stocks (using history as our guide) is about 20.2 percent. Hence, the variance of portfolio returns is 0.202 squared, or 0.040804 for a well-diversified portfolio.

Is variance and volatility the same?

While variance captures the dispersion of returns around the mean of an asset in general, volatility is a measure of that variance bounded by a specific period of time.

How do you calculate variance of return in Excel?

- Find the mean by using the AVERAGE function: =AVERAGE(B2:B7) …

- Subtract the average from each number in the sample: …

- Square each difference and put the results to column D, beginning in D2: …

- Add up the squared differences and divide the result by the number of items in the sample minus 1:

How do you calculate expected return and volatility for a stock portfolio?

Expected return measures the mean, or expected value, of the probability distribution of investment returns. The expected return of a portfolio is calculated by multiplying the weight of each asset by its expected return and adding the values for each investment.