How do you record interest in notes receivable

Dylan Hughes

Published Apr 29, 2026

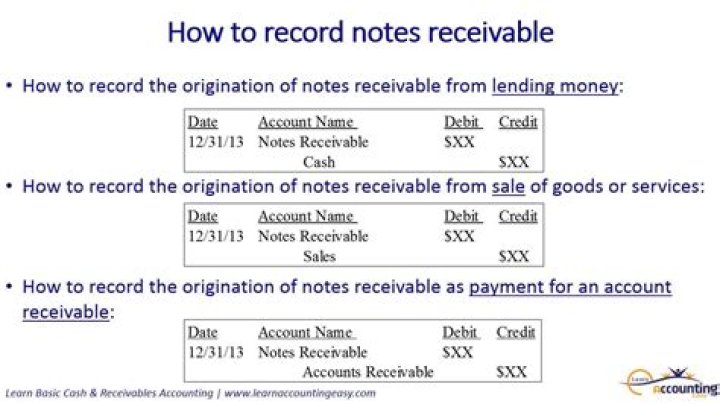

You must record the revenue you’re owed in your books. To record the accrued interest over an accounting period, debit your Accrued Interest Receivable account and credit your Interest Revenue account. This increases your receivable and revenue accounts.

Is interest included in notes receivable?

Stated interest: A note receivable generally includes a predetermined interest rate; the maker of the note is obligated to pay the interest amount due, in addition to the principal amount, at the same time that they pay the principal amount.

How do you account for a note receivable?

The payee should record the interest earned and remove the note from its Notes Receivable account. Thus, the payee of the note should debit Accounts Receivable for the maturity value of the note and credit Notes Receivable for the note’s face value and Interest Revenue for the interest.

How do you record interest on notes payable?

Interest that has occurred, but has not been paid as of a balance sheet date, is referred to as accrued interest. Under the accrual basis of accounting, the amount that has occurred but is unpaid should be recorded with a debit to Interest Expense and a credit to the current liability Interest Payable.What is the journal entry for interest received?

As the normal accounting rule, ‘debit the receiver, credit the giver’ as the interest is being received we credit it. Therefore making the entry complete, Cash account debited and interest account credited.

Is interest receivable an accrual?

Accrued interest on notes receivable is likely to be reported as a current asset such as Accrued Interest Receivable or Interest Receivable. The accrued interest receivable is a current asset if the interest amount is expected to be collected within one year of the balance sheet date.

Where does interest receivable go on balance sheet?

As long as it can be reasonably expected to be paid within a year, interest receivable is generally recorded as a current asset on the balance sheet.

Do notes payable have interest?

Notes payable almost always require interest payments. The interest owed for the period the debt has been outstanding that has not been paid must be accrued. Accruing interest creates an expense and a liability.How do you record principal and interest?

Generally, the interest payment is related to the principal amount that is owed to the lender. Whenever a principal payment occurs, the balance of the principal amount owed will decrease. Therefore, the next interest payment will be smaller than the previous interest payment.

Where can I record interest expense?You can find interest expense on your income statement, a common accounting report that’s easily generated from your accounting program. Interest expense is usually at the bottom of an income statement, after operating expenses. Sometimes interest expense is its own line item on an income statement.

Article first time published onWhat is the difference between accounts receivable and notes receivable?

Accounts receivable are amounts that customers owe the company for normal credit purchases. Notes receivable are amounts owed to the company by customers or others who have signed formal promissory notes in acknowledgment of their debts.

How do you record loans interest and receivables?

When you take out a loan or line of credit, you owe interest. You must record the expense and owed interest in your books. To record the accrued interest over an accounting period, debit your Interest Expense account and credit your Accrued Interest Payable account. This increases your expense and payable accounts.

Is interest received a DR or CR?

Accrued Interest Payable To account for interest payable at the end of an accounting period, debit the amount due as an expense on the income statement. … In the example, debit the interest payable account with $21.92 and the credit current liabilities account with the same amount.

What is interest received example?

A very simple example of interest income that happens every day is when an individual deposits money into a savings account and decides to leave it untouched for several months or years. The money won’t just sit idly in his account, because the bank will use it to lend money to borrowers.

Is interest receivable part of accounts receivable?

Accounts receivable is an informal, short-term payment and usually no interest, whereas notes receivable is a legal contract, long-term payment, and usually has interest.

What are interest receivable and fees receivable accounts?

Interest receivable refers to the interest that has been earned by investments, loans, or overdue invoices but has not actually been paid yet. … As long as it can be reasonably expected to be paid within a year, interest receivable is generally recorded as a current asset on the balance sheet.

Is accrued interest the same as interest receivable?

Accrued interest is the accumulated interest on your loan that the lender has charged but that hasn’t been paid. … For your lender, the amount of interest that it has recognized as revenue but hasn’t received in cash from your business is accrued interest receivable, which is an asset.

How do you separate principal and interest?

Divide your interest rate by the number of payments you’ll make in the year (interest rates are expressed annually). So, for example, if you’re making monthly payments, divide by 12. 2. Multiply it by the balance of your loan, which for the first payment, will be your whole principal amount.

Does interest expense include principal?

Interest expense is a non-operating expense shown on the income statement. It represents interest payable on any borrowings – bonds, loans, convertible debt or lines of credit. It is essentially calculated as the interest rate times the outstanding principal amount of the debt.

How does principal and interest work?

In a principal + interest loan, the principal (original amount borrowed) is divided into equal monthly amounts, and the interest (fee charged for borrowing) is calculated on the outstanding principal balance each month. This means the monthly interest amount declines over time as the outstanding principal declines.

How are notes payable recorded on the balance sheet?

When repaying a loan, the company records notes payable as a debit entry, and credits the cash account, which is recorded as a liability on the balance sheet. … This amount will be recorded in the interest expense account as a debit entry, and the same amount will be appear in the interest payable account as a credit.

Is interest payable a liability?

Interest payable is a liability, and is usually found within the current liabilities section of the balance sheet. The associated interest expense that comprises interest payable is stated on the income statement for the amount applicable to the period whose results are being reported.

How is interest expense calculated?

The simplest way to calculate interest expense is to multiply a company’s total debt by the average interest rate on its debts. If a company has $100 million in debt with an average interest rate of 5%, then its interest expense is $100 million multiplied by 0.05, or $5 million.

How are interest expense and interest paid reported?

First, interest expense is an expense account, and so is stated on the income statement, while interest payable is a liability account, and so is stated on the balance sheet. Second, interest expense is recorded in the accounting records with a debit, while interest payable is recorded with a credit.

What is interest receivable?

Interest receivable is the amount of interest that has been earned, but which has not yet been received in cash.

Why might a business prefer a note receivable to an account receivable?

An account receivable is a simple promise to repay the merchant, and a note receivable is a formal financial instrument that establishes a contract to repay the merchant. A business may prefer a note receivable because it is easier to make the client pay for the purchase when the note is presented.

Is notes receivable a quick asset?

The Basics of Quick Assets Cash and cash equivalents are the most liquid current asset items included in quick assets, while marketable securities and accounts receivable are also considered to be quick assets. Quick assets exclude inventories, because it may take more time for a company to convert them into cash.