What is better interest only or repayment

Lily Fisher

Published Apr 17, 2026

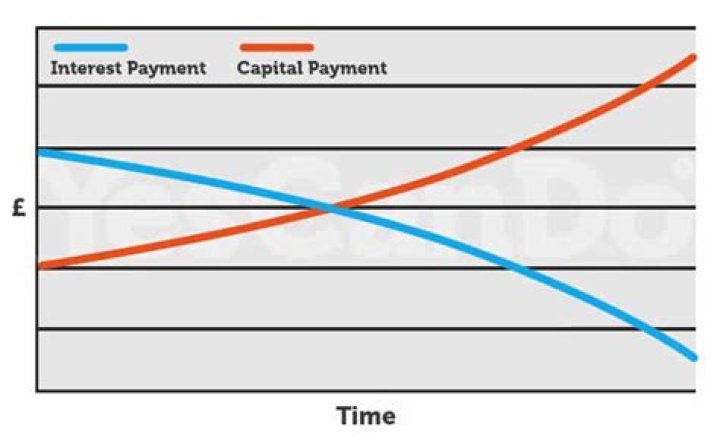

With a repayment mortgage, every month you pay back both the interest on your mortgage AND some of the loan itself. … With an interest-only mortgage, you only pay back the interest on your loan. This means your monthly payments are much lower, but you will still need to pay off the loan at the end of the mortgage term.

Are interest only loans a good idea?

If you’re interested in keeping your month-to-month housing costs low, an interest-only loan may be a good option. Common candidates for an interest-only mortgage are people who aren’t looking to own a home for the long-term — they may be frequent movers or are purchasing the home as a short-term investment.

What is a disadvantage of an interest-only mortgage?

Disadvantages. Interest-only loans don’t build equity. Equity is built through making full mortgage payments. Interest-only loans cost more over time. Interest-only loans cost more than other popular mortgage options such as ARMs or fixed-rate mortgages.

What is the difference between a repayment mortgage and interest only?

With an interest-only mortgage, your monthly payments only cover the interest charged on your loan. With a repayment mortgage, your monthly payments also go towards the initial sum you borrowed.Why are interest only loans bad?

Disadvantages of Interest-Only Loans They often cannot afford the higher payment when the teaser rate expires. Others may not realize they haven’t got any equity in the home and if they sell it, they get nothing. The second disadvantage occurs for those who are counting on a new job to afford the higher payment.

Is it easier to get an interest-only mortgage?

Consider part repayment and part interest-only Those who have a repayment shortfall and are unable to borrow the full amount they need on interest-only can, with many mortgage lenders, split the loan – taking some on interest-only and the rest on repayment. This can make interest-only mortgages easier to get.

Can I sell my house if I have an interest-only mortgage?

Sell the property You can of course sell a property to repay an interest-only mortgage. This is more common among those who buy to let. If you are lucky, the property price will cover the whole loan amount with some left over – but if you are unlucky and run into negative equity, you may have to cover a shortfall.

What happens at the end of an interest-only loan?

Interest-only payments don’t last forever. … The loan eventually converts to an amortizing loan with higher monthly payments. You pay the principal and interest with each payment. You make a significant balloon payment at the end of the interest-only period.What is the point of interest-only mortgage?

An interest-only mortgage allows you to pay just the interest charged each month for the term of the loan. You don’t have to repay the amount you’ve borrowed until the end of the term.

How long can u have an interest-only loan?How long can I stay on an interest-only mortgage? Bank policies vary. Typically the banks will allow interest-only for 2 years for own home and 5 years for investment property.

Article first time published onWhat happens after interest-only mortgage ends?

When an interest-only mortgage ends, you have to repay all the amount you borrowed. The money to repay it can come from three sources: savings or investments; by getting a new mortgage; or.

Is interest only good for first time home buyers?

Interest-only mortgages are beneficial for first-time home buyers. Many new homeowners struggle during the first year of ownership because they are not accustomed to paying mortgage payments, which are generally higher than rental payments.

What is a 10 year interest-only mortgage?

An interest-only mortgage requires payments just of the interest — the “cost of money” — that a lender charges. You’re not paying back any of the borrowed money (the principal). … These home loans are usually structured as adjustable-rate mortgages and frequently have terms of up to 10 years.

Can you switch from interest-only mortgage to repayment?

Yes, this is possible, as long as your mortgage lender approves you for a repayment mortgage. Switching to a repayment mortgage from an interest-only mortgage can be a good option for many borrowers and there are plenty of lenders who allow this.

Can you overpay an interest-only mortgage?

You can make overpayments for both repayment and interest-only mortgages, so it doesn’t matter what type of mortgage you currently have.

Can you remortgage at the end of an interest-only mortgage?

What happens when my interest-only mortgage ends, can I remortgage? Once your original mortgage comes to a close, if you can’t afford to repay all the capital you can either ask your current lender to extend the mortgage term or remortgage to a new lender.

Can I get an interest-only mortgage at 60?

While there’s no minimum age requirement, retirement interest-only mortgages are generally aimed at older borrowers, such as the over 55s, over 60s and pensioners who might find them easier to qualify for than a typical interest-only mortgage.

What is better interest only or principal and interest?

By paying P&I, you’re paying off the mortgage earlier in the term so you end up paying less in interest. … Reduced interest rates: Making principal and interest repayments makes you a lower risk than a borrower making interest only repayments so banks are willing to offer you cheaper interest rates.

Can I change interest only?

Yes. Most lenders will be open to letting you change from a repayment mortgage to an interest-only mortgage. However, they’ll want to do some strict checks before they decide for sure, as they’ll need to be confident they’re going to get their money back!

What's the oldest age you can get a mortgage?

Many lenders impose an age cap at 65 – 70, but will allow the mortgage to continue into retirement if affordability is sufficient. Lender choices become more limited, but some will cap at age 75 and a handful up to 80 if eligibility criteria are met. Term lengths may be restricted.

Who would be interested in an interest only mortgage?

It is a niche product, best suited for borrowers with strong cash flow and good credit and often for home buyers looking for a short-term loan — typically from five to seven years. Many interest-only mortgages are also jumbo loans, for higher-priced properties that don’t meet conventional loan standards.

What is a 40 year interest only mortgage?

A 40-year mortgage means that if you made all payments as scheduled without making extra or bigger payments toward the principal to pay it off sooner, it would take 40 years to pay off the home. More traditional mortgages come in terms anywhere between 8 – 30 years. … They may also be adjustable-rate mortgages (ARMs).

Can you change from principal and interest to interest only?

You can change between principal and interest repayments and interest-only repayments to estimate the different interest charges.