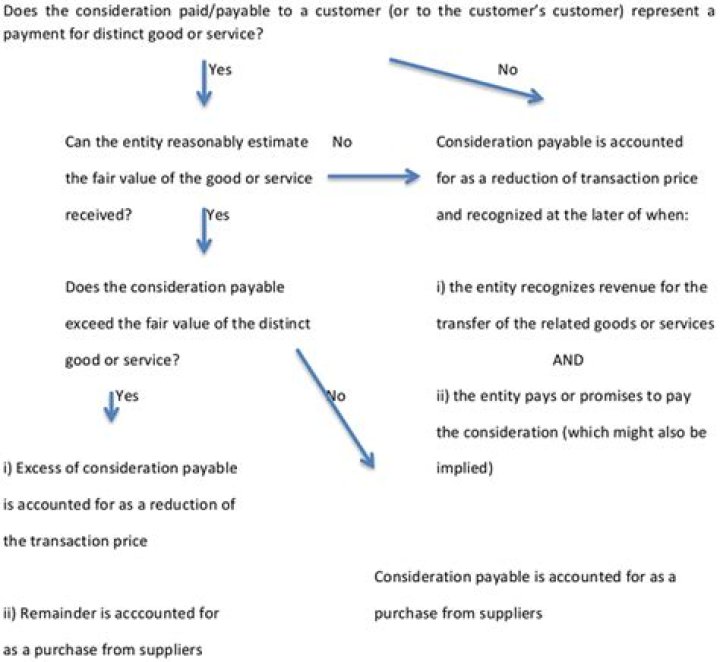

What is consideration payable to a customer

Ava Hall

Published Feb 23, 2026

Consideration payable to a customer includes cash amounts that an entity pays, or expects to pay, to the customer (or to other parties that purchase the entity’s goods or services from the customer).

What is consideration paid?

Consideration is a payment made by one party to another in exchange for the transfer of something of value. It must be of value to both parties entering into a transaction. Several examples of consideration are as follows: … Paying cash in exchange for a right of first refusal for real estate.

What is variable consideration?

Variable consideration includes discounts, credits, rebates, performance bonus, penalties, sales returns, refunds, price concessions, incentives, etc. The transaction price includes such variable considerations, whether explicitly stated in the contract or implicitly stated.

What is an identifiable benefit?

The term “identifiable benefit” is described as a good or service that is sufficiently separable from the customer’s purchase of the entity’s goods or services such that the entity could have entered into an arrangement with a party that does not purchase the entity’s goods or services and receive the same benefit.What are the 5 steps of ASC 606?

- Identify the contract with a customer. …

- Identify the Performance Obligation in the contract. …

- Determine the transaction price. …

- Allocate the transaction price. …

- Recognize Revenue.

What is consideration cost?

The term “consideration” is a concept in English law that refers to the price paid in exchange for the fulfillment of a promise. The court in the case of Currie v Misa defined consideration as a right, interest, profit, detriment, loss, or responsibility.

What is consideration give example?

When the promisor receives consideration simultaneously with his promise, the consideration is termed as Present Consideration. Example: A purchased goods from a shopkeeper of the worth of ` 10,000 A pays money to the shopkeeper immediately. Consideration is “Present”.

How do you recognize revenue under Aspe?

Entities recognize revenue from service and long-term contracts as activities are performed, using one of two methods: Completed contract is a method of accounting that recognizes revenue only when the sale of goods or the rendering of services under a contract is completed or substantially completed.Is the amount of consideration that a company expects to receive from a customer?

The transaction price is the amount of consideration that a company expects to receive from a customer in exchange for transferring a good or service.

What is fixed consideration?Fixed Consideration means the aggregate sum (a) the Cash Consideration, and (b) the Stock Consideration.

Article first time published onWhat is non cash consideration?

Non-cash considerations can typically be defined as consideration which is received or receivable by the customer which is in a form other than cash.Examples of non-cash considerations typically include: ➢ Shares. ➢ Material, equipment and labor.

Which of the following is an example of a variable consideration?

Examples of variable consideration include: Discounts, rebates, refunds and credits; Price concessions, incentives and performance bonuses; Penalties; and.

What is the difference between 605 and 606?

ASC 606 focuses on the transfer of control rather than the satisfaction of obligations prescribed by ASC 605. It’s a principles-based framework that introduces more judgement into the revenue recognition process. Its core principles are focused on the nature of the promises in a contract.

What are the 5 steps of recognizing revenue?

- Step 1 – Identify the Contract. …

- Step 2 – Identify Performance Obligations. …

- Step 3 – Determine the Transaction Price. …

- Step 4 – Allocate the Transaction Price. …

- Step 5 – Recognize Revenue.

What is revenue recognition principle?

The revenue recognition principle, a feature of accrual accounting, requires that revenues are recognized on the income statement in the period when realized and earned—not necessarily when cash is received. … Earned revenue accounts for goods or services that have been provided or performed, respectively.

What are the 4 types of consideration?

The various types of consideration are (1) a promise, (2) an act other than a promise, (3) forbearance, (4) a change in a legal relation of the parties, (5) money, or (6) other property.

What is consideration simple words?

In the legal system, the term consideration in contract law refers to something of value given to someone in return for goods, services, or some other promise. … In simple terms, consideration is the basic reason a party enters into a legal contract.

What are the six types of consideration?

- 1.An offer made by the offerer.

- 2.An acceptance of the offer by the offeree.

- Consideration in the form of money or a promise to do or not do something.

- Mutuality between parties to carry out the promises of the contract.

- Capacity of both parties in mind and age.

- Legality of terms and conditions.

How is consideration amount calculated?

Net Worth or Net Assets Method: Under this method, purchase consideration is calculated by adding up the values of various assets taken over by the purchasing company and then deducting there from the values of various liabilities taken over by the purchasing company.

Why consideration is important in business?

Consideration is one of the most important parts of a contract because it states why each party is joining the agreement. Consideration can be the exchange of money for products or services, or it can be a trade of one type of product for another type of product. … Without it, the contract would be considered a gift.

Why is consideration needed?

When forming a contract, consideration is needed in order to make the agreement a formal, valid contract. … Consideration is needed so that both parties incur some sort of burden or obligation in the agreement. Without consideration, the exchange would likely be classified as a gift.

What criteria must be present for consideration due to a customer to be treated as a separate transaction involving a purchase of goods or services from the customer?

Each promised good or service, or bundle of related goods or services, must meet the following two criteria to be considered a distinct obligation: (1) the customer can derive benefit from the offering either on its own or with readily available resources, and (2) the offering is able to be separated from the other …

What is a transaction price in a contract with customer?

The Transaction Price is the amount of consideration an entity expects to receive for the transfer of goods or services to the customer. The amount can be fixed, variable, or a combination of both. Transaction Price is allocated to the identified performance obligations in the contract.

Can the customer benefit from the good or service either on its own or together with other resources that are readily available to the customer?

A good or service is distinct if: The customer can benefit from the good or service either on its own or together with other resources that are readily available to the customer (that is, the good or service is capable of being distinct).

What is the difference between IFRS and ASPE?

ASPE was designed for private companies; IFRS is to be applied by public companies and other publicly accountable enterprises. However, private companies may choose to use IFRS. They should adopt IFRS when a business need requires it.

Is service fees a revenue?

Service Revenue is income a company receives for performing a requested activity. … This means all fees for services performed to date can be included in an income statement, even if not all the bills have been sent out to clients yet.

When should expenses be recognized Aspe?

The expense recognition principle states that expenses should be recognized in the same period as the revenues to which they relate. If this were not the case, expenses would likely be recognized as incurred, which might predate or follow the period in which the related amount of revenue is recognized.

What is contract Java?

The contract of a class or interface, in Java or any other OO language, generally refers to the publicly exposed methods (or functions) and properties (or fields or attributes) of that class interface along with any comments or documentation that apply to those public methods and properties.

Who are competent to contract?

Every person is competent to contract who is of the age of majority according to the law to which he is subject1 , and who is of sound mind and is not disqualified from contracting by any law to which he is subject. 1. See the Indian Majority Act, 1875 (9 of 1875).

What does executed version mean?

Executed Document In Real Estate To execute a document means to sign it. People who refer to an executed real estate contract actually mean that the document – the paper or digital copy of the contract – has been signed.

Is variable consideration a performance obligation?

Variable consideration is generally allocated to all performance obligations in a contract based on their relative standalone selling prices.