What loan fees are tax deductible

Rachel Hunter

Published Mar 24, 2026

The mortgage interest deduction allows you to deduct the interest you pay on your mortgage each year. You can deduct a total of $1 million or $750,000 in interest depending on whether you bought your home before or after Dec. 16, 2017. You can also deduct the property taxes you pay each year, up to $10,000.

Are loan processing fees tax deductible?

Fortunately, YES. You can deduct your loan processing fees from your tax returns. Unfortunately, many taxpayers aren’t aware that these charges are tax-deductible according to law. The costs are considered interest on the loan and hence you can claim their deduction.

What loan expenses can I deduct?

Though personal loans are not tax deductible, other types of loans are. Interest paid on mortgages, student loans, and business loans often can be deducted on your annual taxes, effectively reducing your taxable income for the year.

Which loan origination fees are tax deductible?

4. Origination Fees. The IRS classifies mortgage origination fees as points. You can deduct your loan origination fees, even if the seller pays them.Are loan fees an expense?

The loan fees are amortized through Interest expense in a Company’s income statement over the period of the related debt agreement. … There are also certain disclosures relating to capitalized loan fees which are required to be made in a Company’s footnotes.

Where do origination fees go on tax return?

Loan origination fees (also called points) get entered under the Mortgage Interest section of Turbotax and are placed on Schedule A along with your other mortgage interest on Line 10.

Are escrow fees tax deductible?

Yes, as long as the payment has been made it is still deductible. You will deduct the amount that your escrow paid, not the amount that you pay into escrow.

Are closing costs tax deductible in 2021?

Can you deduct these closing costs on your federal income taxes? In most cases, the answer is “no.” The only mortgage closing costs you can claim on your tax return for the tax year in which you buy a home are any points you pay to reduce your interest rate and the real estate taxes you might pay upfront.Are appraisal fees deductible?

Generally, appraisal fees will be deductible on your Schedule C or Schedule E if the appraisal is conducted for business reasons. If you are buying or selling a personal property appraisal fees are not deductible. … Appraisal fees paid to determine the value of damaged business property are usually deductible.

Can personal loans be deductible?A personal loan is not considered a part of your income and is, therefore, not taxable. There are no tax benefits on personal loans. Only certain loans which are secured and for specific purposes have tax benefits, such as a home loan or secured business loans.

Article first time published onDo I have to report a personal loan on my taxes?

Personal loans generally aren’t taxable because the money you receive isn’t income. Unlike wages or investment earnings, which you earn and keep, you need to repay the money you borrow. Because they’re not a source of income, you don’t need to report the personal loans you take out on your income tax return.

Is a loan taxable?

Because a loan means you’re borrowing money from a lender or bank, they aren’t considered income. Income is defined as money you earn from a job or an investment. Not only are all loans not considered income, but they are typically not taxable.

How do you account for loan costs?

Loan costs may include legal and accounting fees, registration fees, appraisal fees, processing fees, etc. that were necessary costs in order to obtain a loan. If the loan costs are significant, they must be amortized to interest expense over the life of the loan because of the matching principle.

Are loan fees considered interest?

Lenders often include fees in loan transactions in addition to an interest rate. Typically such fees are not considered interest, as they compensate the lender for various services or commitments provided under the loan agreements.

What loan fees should be capitalized?

Capitalized Loan Fees means, with respect to the REIT and any Consolidated Entity, and with respect to any period, (a) any up-front, closing or similar fees paid by such Person in connection with the incurring or refinancing of Indebtedness during such period and (b) all other costs incurred in connection with the …

Is mortgage interest tax deductible?

That means this tax year, single filers and married couples filing jointly can deduct the interest on up to $750,000 for a mortgage if single, a joint filer or head of household, while married taxpayers filing separately can deduct up to $375,000 each. … All of the interest you pay is fully deductible.

Is mortgage insurance tax deductible?

Yes, through tax year 2020, private mortgage insurance (PMI) premiums are deductible as part of the mortgage interest deduction.

Are sellers closing costs tax deductible?

Sellers can deduct closing costs such as real estate commissions, legal fees, transfer taxes, title policy fees, and deed recording fees to lower the profit and lower the potential taxes owed.

Why is my mortgage interest not deductible?

If the loan is not a secured debt on your home, it is considered a personal loan, and the interest you pay usually isn’t deductible. Your home mortgage must be secured by your main home or a second home. You can’t deduct interest on a mortgage for a third home, a fourth home, etc.

Are loan appraisal fees amortized?

Points paid upon refinancing of a primary residence or purchase of investment property is amortized over the life of the loan. 803. Appraisal fee. … These items must be amortized over the life of the loan.

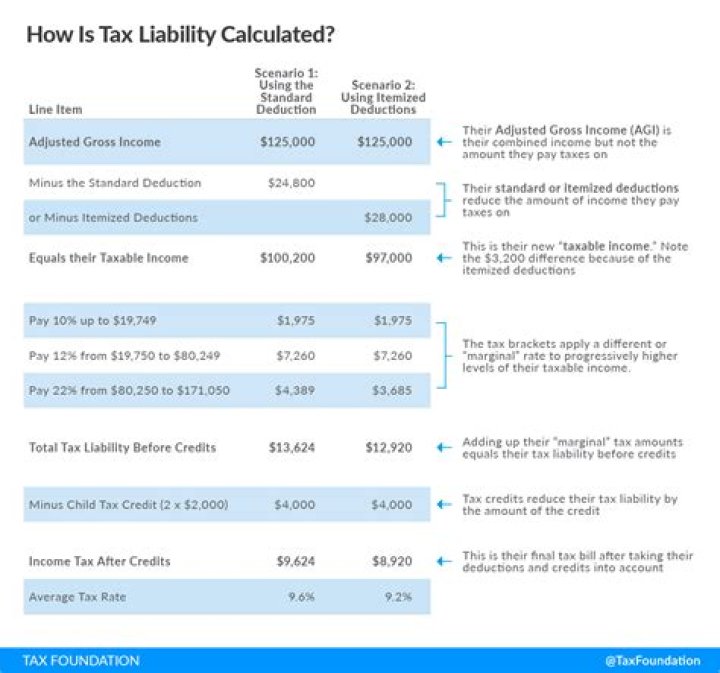

What is the 2021 standard deduction?

Filing StatusStandard Deduction 2021Standard Deduction 2022Single; Married Filing Separately$12,550$12,950Married Filing Jointly & Surviving Spouses$25,100$25,900Head of Household$18,800$19,400

Is mortgage deductible from rental income?

Your mortgage payments cannot be used as an expense on a residential rental property. You can not deduct the mortgage payment;You can deduct the mortgage interest. … You will also have other expenses that you can claim, insurance, taxes and repairs.

How do I write off unamortized loan fees?

- Manually adjust the current amortization to reflect the full amount of the balance.

- Next year, delete this asset worksheet. To delete forms next year, from the left menu, select Tax Tools> Tools>Delete a Form>Scroll to the Asset Worksheet and click Delete.

Are business loan origination fees tax deductible?

If you pay off a loan to the original lender with the funds from a second loan is not a business expense. This means the interest you are paying to the first lender is not tax deductible. … The points and loan origination fees are not considered business expenses and cannot be deducted.

Can you write off a loan to a friend?

Generally, to deduct a bad debt, you must have previously included the amount in your income or loaned out your cash. … If you lend money to a relative or friend with the understanding the relative or friend may not repay it, you must consider it as a gift and not as a loan, and you may not deduct it as a bad debt.

Does a loan count as income?

Borrowers can use personal loans for all kinds of purposes, but can the Internal Revenue Service (IRS) treat loans like income and tax them? The answer is no, with one significant exception: Personal loans are not considered income for the borrower unless the loan is forgiven.

Can you loan money to a friend tax free?

In most cases, you won’t have to pay taxes for a “loan” the IRS deemed a gift. You only owe gift tax when your lifetime gifts to all individuals exceed the Lifetime Gift Tax Exclusion. For tax year 2017, that limit is $5.49 million. For most people, that means they’re safe.

Are loans included in gross receipts?

This includes revenue from the sale of products or services, interest, dividends, rents, royalties, fees or commissions, reduced by returns and allowances but excluding net capital gains and losses. Importantly, gross receipts do not include forgiven PPP loan proceeds or economic injury disaster loan (EIDL) advances.

Are loan origination fees interest income?

Essentially, the FASB requires that loan origination fees and costs should be deferred and (generally) amortized as a component of interest income over the life of the loan. … In general, they are the costs associated with originating a specific loan.

Are loan fees intangible assets?

For tax purposes, intangible assets generally need to be amortized over a specified period of time, depending on the type of asset or life of the asset. … Loan fees are amortized over the life of the loan. Intangible assets are generally shown in the other asset section of a balance sheet as one of the last items.

What are FAS 91 fees?

FAS 91 Fees means any fees received and deferred in accordance with Statement of Financial Accounting Standards No. 91, net of associated deferred costs.