When you dont have to start paying your college loans back until after you graduate your loans are quizlet

Rachel Hunter

Published Mar 03, 2026

no, Typically, you can wait for six months after you leave school before you have to start paying back these loans. This is called a grace period. you aren’t expected to make payments on these loans while you’re in school. In fact, you have six months after you graduation to start making payments.

What loans do not have to be repaid until after you graduate from college?

Federal loans don’t have to be repaid until you graduate or drop below half-time status as a student. Many private loans ask for repayment while you’re still in school.

Which term is defined as a loan given to students to help pay for education related expenses?

Which term is defined as a loan given to students to help pay for education-related expenses? student loan.

Do student loans often don't require you to start paying them back until after you've completed the course?

Terms in this set (30) True or False: Student loans often don’t require you to start paying them back until after you’ve completed the course(s). True. Most of the time you will 3-6 months after you are no longer enrolled in college before you will have to start paying students loans back.Is it possible to graduate college with no debt?

Given that the average student leaves school owing over $28,000, graduating without debt may appear impossible. The 30% of students that do graduate without a loan demonstrate that it is possible to complete college debt free — it just takes a lot of creative thinking and bit of extra work.

What are the 4 types of loans you can take out for college?

There are four main types of loans available to undergraduate students: Subsidized, Unsubsidized, Parent PLUS, and Private.

What types of loans are available to pay for college?

There are three types of student loans: federal loans, private loans and refinance loans once you leave school. Federal loans are provided by the government, while banks, credit unions and states make private loans and refinance loans.

What is the maximum student loan amount?

Undergraduates can borrow up to $12,500 annually and $57,500 total in federal student loans. Graduate students can borrow up to $20,500 annually and $138,500 total.How long after college do you have to start paying loans?

For most federal student loan types, after you graduate, leave school, or drop below half-time enrollment, you have a six-month grace period (sometimes nine months for Perkins Loans) before you must begin making payments.

Can you repay student loans all at once?Yes, you can pay your student loan in full at any time. If you are financially able to do so, it may make sense for you to pay off your student loans early. Lenders typically call this “prepayment in full.” Generally, there are no penalties involved in paying off your student loans early.

Article first time published onDo you have to pay back FAFSA?

FAFSA is not the financial aid itself, so you do not have to pay it back. … Federal student aid that is awarded based on the FAFSA includes the Federal Pell Grant, Federal Work-Study and federal student loans. The FAFSA is also used to award state grants and institutional grants from colleges and universities.

Can FAFSA cover full tuition?

The financial aid awarded based on the FAFSA can be used to pay for the college’s full cost of attendance, which includes tuition and fees. … For most students, there will not be enough financial aid to cover the full cost of tuition, unless the parents borrow a Federal Parent PLUS loan.

Is FAFSA a loan or grant?

The FAFSA is not a loan. It is an application form. However, you can use the FAFSA to apply for financial aid and federal student loans. The FAFSA, or Free Application for Federal Student Aid, is used to apply for several types of financial aid, including grants, student employment and federal student loans.

How can I get out of debt-free college?

- Pay Cash for Your Degree. …

- Apply for Aid. …

- Choose an Affordable School. …

- Go to Community College First. …

- Consider Directional Schools. …

- Explore Trade Schools. …

- Apply for Scholarships. …

- Get Grants.

How do I get out of college debt?

- Make additional payments.

- Establish a college repayment fund.

- Start early with a part-time job in college.

- Stick to a budget.

- Consider refinancing.

- Apply for loan forgiveness.

- Lower your interest rate through discounts.

- Take advantage of tax deductions.

How can I go to college debt-free?

- Going to College Without Debt.

- 1) Earn College Credits In High School.

- 2) Apply for A LOT of Scholarships.

- 3) Negotiate With Financial Aid.

- 4) Work A Part Time Job.

- 5) Get A Useful Degree.

- 6) Save In A 529 Plan.

- 7) Choose Untraditional Schooling.

What is the average student loan debt in 2020?

Student Loans in 2020 & 2021: A Snapshot30%Percentage of college attendees taking on debt, including student loans, to pay for their education$38,792Average amount of student loan debt per borrower5.7%Percentage of student debt that was 90+ days delinquent or in default

Which federal loan type is available for parents?

The U.S. Department of Education makes Direct PLUS Loans to eligible parents through schools participating in the Direct Loan Program. (We also offer PLUS loans for graduate or professional students.) A Direct PLUS Loan is commonly referred to as a parent PLUS loan when made to a parent borrower.

What is a college loan called?

If you apply for financial aid, you may be offered loans as part of your school’s financial aid offer. A loan is money you borrow and must pay back with interest. … Loans made by the federal government, called federal student loans, usually have more benefits than loans from banks or other private sources.

How can I pay for college without fafsa?

- Complete Your FAFSA. …

- Qualify for Merit Scholarships. …

- Apply for Private Scholarships. …

- Apply for ROTC Scholarships. …

- Attend a Community College. …

- Earn College Credit in High School For FREE. …

- Get a Job, or Two. …

- Education is a Gift.

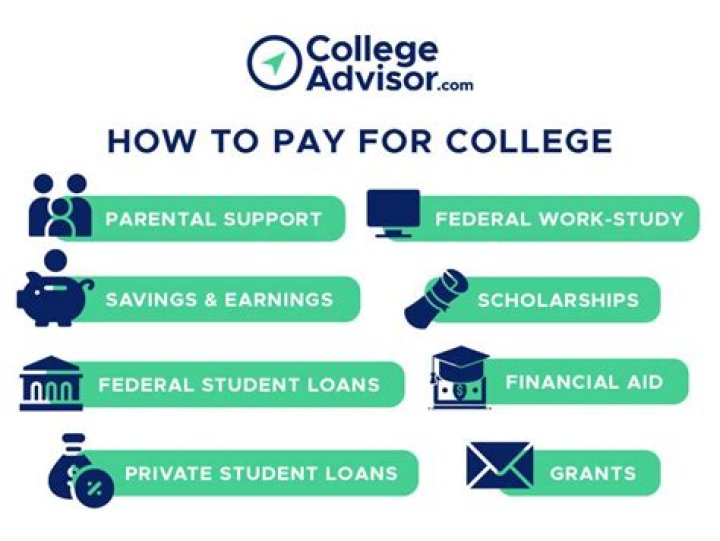

How do you pay for college?

- Fill out the FAFSA. …

- Search for scholarships. …

- Choose an affordable school. …

- Use grants if you qualify. …

- Get a work-study job. …

- Tap your savings. …

- Take out federal loans if you have to. …

- Borrow private loans as a last resort.

What is a grant for college?

Grants for college are a form of financial aid that does not usually get repaid. They cover a variety of education-related expenses, such as tuition and fees, room and board, and books and supplies.

At what point must you start repaying your college loans?

You begin repaying most federal student loans six months after you leave college or drop below half-time enrollment.

What happens if you can't repay the loans?

If You Don’t Pay If you stop paying on a loan, you eventually default on that loan. The result: You’ll owe more money as penalties, fees, and interest charges build up on your account. Your credit scores will also fall.

What is a loan forgiveness program?

The Public Service Loan Forgiveness (PSLF) Program forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer.

What is the maximum income to qualify for financial aid 2021?

For 2021, if your family’s adjusted gross annual income is less than $27,000 and your EFC is calculated at zero, then you may receive the maximum amount in Pell Grant funding of $6,495 per year. You can determine your Pell Grant funding based on Cost of Attendance and Expected Family Contribution.

What is the full amount of Pell Grant?

The maximum Federal Pell Grant award is $6,495 for the 2021–22 award year (July 1, 2021, to June 30, 2022). your plans to attend school for a full academic year or less.

Do student loans cover all tuition?

Student loans are intended to pay for college, but education costs include more than tuition. … You’re limited to borrowing the school’s cost of attendance — that’s tuition and fees, books and supplies, room and board, transportation, and personal expenses —minus any aid you receive.

How do you pay off old student loans?

- Teacher Loan Forgiveness. …

- Public Service Loan Forgiveness (PSLF) …

- Income-Driven Repayment (IDR) Plan. …

- Military Service. …

- AmeriCorps. …

- Other Options.

How many days after missing a student loan payment do your loans go into default?

While federal student loans don’t go into default until after 270 days of past-due payments, borrowers with private student loans are beholden to the rules of their loan providers.

What if I pay my student loan off early?

Pros. Pay less over the life of the loan: Because your student loan, like most other debt, accrues interest when you carry a balance, it’s cheaper if you pay off the loan earlier. It gives the debt less time to accumulate interest, which means that you’ll pay less money in the long run.