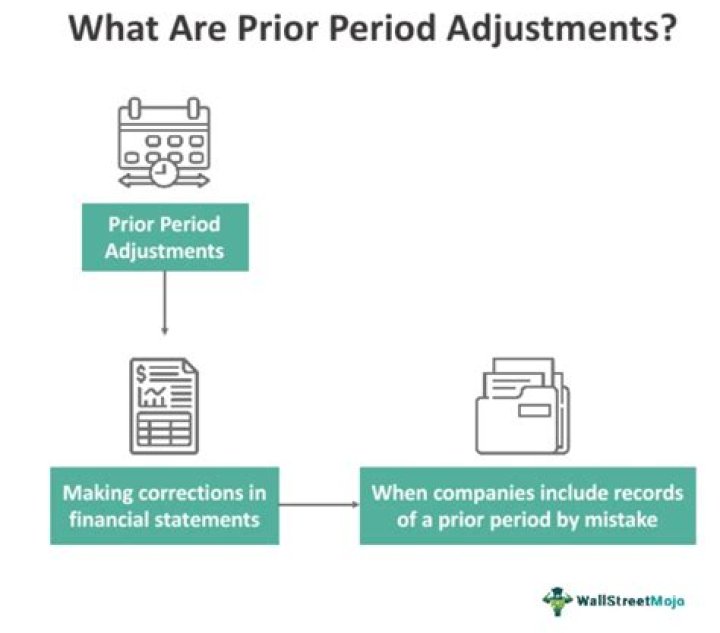

Where are prior period adjustments reported

Andrew Campbell

Published May 20, 2026

The most common example is the correction of an error from a prior year. When such a correction is made, it is reported in the current period’s statement of retained earnings rather than in the current period’s income statement.

Where should a prior period adjustment be reported?

Since balance sheet and income statement effects of these errors have already occurred, the adjustment should be made to the retained earnings or equity account on the statement of retained earnings.

Do prior period adjustments go on the income statement?

Prior period adjustments are capable of affecting the balance sheet, income statement or even both. If the error affects both, opening retained earnings will be affected and prior period adjustment entry will need to be recorded.

How are prior period adjustments reported on the financial statements?

You should account for a prior period adjustment by restating the prior period financial statements. This is done by adjusting the carrying amounts of any impacted assets or liabilities as of the first accounting period presented, with an offset to the beginning retained earnings balance in that same accounting period.Where are adjustments made to financial statements?

Adjusting entries are made at the end of the accounting period to make your financial statements more accurately reflect your income and expenses, usually — but not always — on an accrual basis.

How do you fix prior year errors?

Prior Period Errors must be corrected Retrospectively in the financial statements. Retrospective application means that the correction affects only prior period comparative figures. Current period amounts are unaffected. Therefore, comparative amounts of each prior period presented which contain errors are restated.

How do you disclose prior period?

The nature and amount of prior period items should be separately disclosed in the statement of profit and loss in a manner that their impact on the current profit or loss can be perceived.

How do you adjust prior year retained earnings?

Correct the beginning retained earnings balance, which is the ending balance from the prior period. Record a simple “deduct” or “correction” entry to show the adjustment. For example, if beginning retained earnings were $45,000, then the corrected beginning retained earnings will be $40,000 (45,000 – 5,000).What is a prior period adjustment and when is this accounting device used?

Terms in this set (162) What is a prior period adjustment, and when is this accounting device used? It is used to fix an error in the previous statements. It is used when someone notices a mistake made previously. Describe the journal entry and financial statement effect of restatements for errors.

What are prior period errors?Prior period errors are omissions from, and misstatements in, an entity’s financial statements for one or more prior periods arising from a failure to use, or misuse of, reliable information that was available and could reasonably be expected to have been obtained and taken into account in preparing those statements.

Article first time published onHow do I create a prior year adjustment in Quickbooks?

- Click the Plus Icon.

- Choose Journal Entry.

- Type in the transaction’s date in the Journal Date field.

- On the first distribution line, in the Accounts field, enter any account listed in the Chart of Accounts.

- Enter the transaction amount in the Debits or Credits column.

What are 2 examples of adjustments?

- Altering the amount in a reserve account, such as the allowance for doubtful accounts or the inventory obsolescence reserve.

- Recognizing revenue that has not yet been billed.

- Deferring the recognition of revenue that has been billed but has not yet been earned.

What adjustments are made at the end of the year?

Examples of Year-End Adjustments Accrual of expenses for which supplier invoices have not yet been received. For example, an interest billing from the bank may arrive late, so the expense is accrued. Accrual of payroll expenses for hours worked that have not yet been paid.

Why adjustments are made to financial statements?

The main purpose of adjusting entries is to update the accounts to conform with the accrual concept. At the end of the accounting period, some income and expenses may have not been recorded or updated; hence, there is a need to adjust the account balances.

How do you record prior year expenses?

Record the expenses as bills, either individually or collectively, as one itemized report, dating them from the beginning of the current fiscal year. In the memo section of the expense report, note that the expenses were from a previous fiscal year.

Under which section are prior period expenses disallowed?

(i) Prior period expenditure and prior period income. (ii) Disallowance made under Section 40(a)(i) of the Act. (iii) Section 10(B) deduction in respect of the turn over for which the sales proceeds were not realized. (iv) The other income as being eligible for deduction under Section 10(B) of the Act.

What does Accounting Standards 5 stands for?

Accounting Standard 5 (AS 5) deals with the classification and disclosure of specific items in the Statement of Profit and Loss. The purpose of AS 5 is to suggest such a classification and disclosure in order to bring uniformity in the preparation and presentation of statement of net profit or loss across enterprises.

Which of the following is a correction of an error that was committed from prior periods?

A prior period error shall be corrected by retrospective restatement except to the extent that it is impracticable to determine either the period-specific effects or the cumulative effect of the error.

What does prior period mean?

Prior Period means the fiscal year of the Relevant Company that coincides with or ends within the fiscal year of the Company immediately preceding the fiscal year of the Company to which the applicable Performance Goal applies.

How do I create corrections in QuickBooks?

- Click Accounting from the left menu, then select Chart of Accounts.

- Find the bank account from the list and click View register.

- Locate and select the transaction you want to change, then hit Edit.

- Change the category or description, then click Save.

- Click Yes to confirm the changes.

Can I adjust retained earnings?

Nonetheless, you can post an adjustment to retained earnings in a prior period in the current period’s retained earnings account to correct the errors. … This entry decreases revenue and retained earnings to reflect the correct financial position of the business, reports Accounting Tools.

How do I adjust a balance sheet in QuickBooks?

- Go to Reports menu at the left panel, then type Invoices and Received Payments.

- Select Customize, then click Change columns link.

- Select A/R Paid, Open Balance, and other columns you want to display in the report. Then, click Run report.

What are the main adjustments?

- Accrued expenses.

- Accrued revenues.

- Deferred expenses.

- Deferred revenues.

What are the four basic types of adjusting entries?

There are four types of account adjustments found in the accounting industry. They are accrued revenues, accrued expenses, deferred revenues and deferred expenses.

What is an in year adjustment?

The In Year Adjustment (IYA) backstory The idea was that HMRC would use third-party information from pension providers and Personal Tax Accounts (PTA) to update tax information throughout the year. … In theory, this would mean that Week-1/Month-1 basis codes would be used less, and tax refunds would be speeded up.

What are end of period adjustments?

End-of-period-adjustments in accounting are journal entries made to the accounts of a business prior to the preparation and distribution of the financial statements for a given accounting period. … End-of-period adjustments are also known as year-end-adjustments, adjusting-journal-entries and balance-day-adjustments.

What is adjustment in account or end of the year adjustment?

These are adjustment which are made in the profit and loss account and balance sheet, thus will ensure that the the final accounts of an organization show the true view of their transaction,they are closing adjustment or amendment made in the book at the end of the accounting period in order to match revenue with …

What are the different types of adjustments?

- Accrued revenues. When you generate revenue in one accounting period, but don’t recognize it until a later period, you need to make an accrued revenue adjustment. …

- Accrued expenses. …

- Deferred revenues. …

- Prepaid expenses. …

- Depreciation expenses.

What are adjustments?

1 : the act or process of adjusting. 2 : a settlement of a claim or debt in a case in which the amount involved is uncertain or full payment is not made. 3 : the state of being adjusted. 4 : a means (such as a mechanism) by which things are adjusted one to another.

What are the 5 adjusting entries?

Adjustments entries fall under five categories: accrued revenues, accrued expenses, unearned revenues, prepaid expenses, and depreciation.