Which accounting principle states that a company should record revenues when they are earned

Ava Hall

Published Mar 29, 2026

The revenue recognition principle, a feature of accrual accounting, requires that revenues are recognized on the income statement in the period when realized and earned—not necessarily when cash is received.

Which accounting principle states that revenue should not be recorded before it is earned?

The revenue recognition principle states that one should only record revenue when it has been earned, not when the related cash is collected.

Which of the following accounting principles states that a company record its expenses in the same time period as the revenue generated by those expenses?

Accrual Accounting and the Matching Principle One of the accrual accounting method’s most vital concepts is the matching principle, which states that any revenues generated must be paired with any related expenses, within the same reporting period in which the profits were earned, in an effort to eliminate confusion.

Which accounting principle states that a company should?

The revenue recognition principle states that: Revenue should be recognized in the period earned. Which accounting principle states that a company should “record revenues when they are earned”?What is revenue recognition principle?

The revenue recognition principle, a key feature of accrual-basis accounting, dictates that companies recognize revenue as it is earned, not when they receive payment. Accurate revenue recognition is essential because it directly affects the integrity and consistency of a company’s financial reporting.

How do you record revenues?

The accrual journal entry to record the sale involves a debit to the accounts receivable account and a credit to sales revenue; if the sale is for cash, debit cash instead. The revenue earned will be reported as part of sales revenue in the income statement for the current accounting period.

When should we record revenue?

Revenue should be recorded when the business has earned the revenue. This is a key concept in the accrual basis of accounting because revenue can be recorded without actually being received. Revenues are realized or realizable when a company exchanges goods or services for cash or other assets.

What are accounting principles?

What Are Accounting Principles? Accounting principles are the rules and guidelines that companies must follow when reporting financial data. The Financial Accounting Standards Board (FASB) issues a standardized set of accounting principles in the U.S. referred to as generally accepted accounting principles (GAAP).Which accounting principle states that a business must record expenses?

Matching principle is the accounting principle that requires that the expenses incurred during a period be recorded in the same period in which the related revenues are earned. This principle recognizes that businesses must incur expenses to earn revenues.

How realization and matching principle is applied to revenue and expense?The matching principle requires that expenses incurred to produce revenue must be deducted from revenue earned in an accounting period to derive net income. … The matching principle also requires that estimates be made, based on experience and economic conditions, for the purpose of providing for doubtful accounts.

Article first time published onWhat are the four GAAP principles?

The four basic constraints associated with GAAP include objectivity, materiality, consistency and prudence.

How do you record revenue in journal entries?

To create the sales journal entry, debit your Accounts Receivable account for $240 and credit your Revenue account for $240. After the customer pays, you can reverse the original entry by crediting your Accounts Receivable account and debiting your Cash account for the amount of the payment.

What accounting principle is a Philippine company should report financial statements in pesos?

Example: Philippine companies are required to report financial statements annually. Monetary Unit Principle – amounts are stated into a single monetary unit. Example: Jollibee should report financial statements in pesos even if they have a store in the United States.

What is a revenue accounting?

In accounting, revenue is the total amount of income generated by the sale of goods and services related to the primary operations of the business. Commercial revenue may also be referred to as sales or as turnover. … Profits or net income generally imply total revenue minus total expenses in a given period.

Why is revenue recognition principle needed?

The revenue recognition principle enables your business to show profit and loss accurately, since you will be recording revenue when it is earned, not when it is received. Using the revenue recognition principle also helps with financial projections; allowing your business to more accurately project future revenues.

Which of the following is considered to be on earned revenue?

Earned revenue are funds where the person providing money will receive a good or service of equal or greater value in exchange. This includes (but is not limited to) ticket sales, payment for services/work, advertising, class/camp/workshop fees, artwork sales, and merchandise fees.

Where are revenues recorded?

Revenues earned from a company’s operations must be recorded in the general ledger, then reported on an income statement every reporting period.

When should a company record earned revenue under accrual accounting quizlet?

Under the accrual basis of accounting, no entry is made until the $2,000 is paid. In cash basis accounting, revenue is recognized when cash is received and expenses are recognized when they are paid. Under accrual basis accounting, revenue is recorded only when cash is received.

Under what basis and principle accrual revenue is recorded?

Accrued revenue is used in accrual accounting where revenue is recorded at the time of sale—even if payment is not yet received. This follows the revenue recognition principle, which requires that revenue be recorded in the period in which it is earned.

When can sales revenues be recorded quizlet?

Recording the sale of merchandise on credit as sales revenue. Revenue is recognized when earned, not upon the collection of cash. – Revenues increase stockholders’ equity through the account Retained Earnings and therefore have credit balances. You just studied 20 terms!

Where do revenues and expenses go on balance sheet?

In short, expenses appear directly in the income statement and indirectly in the balance sheet. It is useful to always read both the income statement and the balance sheet of a company, so that the full effect of an expense can be seen.

How do you identify revenue in accounting?

According to the principle, revenues are recognized when they are realized or realizable, and are earned (usually when goods are transferred or services rendered), no matter when cash is received. In cash accounting – in contrast – revenues are recognized when cash is received no matter when goods or services are sold.

How are revenues and expenses reported on the income statement under cash basis accounting?

Under the accrual basis of accounting (or accrual method of accounting), revenues are reported on the income statement when they are earned. … (Under the cash basis of accounting, revenues are not reported on the income statement until the cash is received.)

How are revenues and expenses reported on the income statement under the cash basis of accounting and the accrual basis of accounting?

How are revenues and expenses reported on the income statement under the cash basis of accounting? Under the cash basis of accounting, revenues are reported in the period in which cash is received, and expenses are reported in the period in which cash is paid.

When should supplies be recorded as an expense?

The cost of office supplies on hand at the end of an accounting period should be the balance in a current asset account such as Supplies or Supplies on Hand. The cost of the office supplies used up during the accounting period should be recorded in the income statement account Supplies Expense.

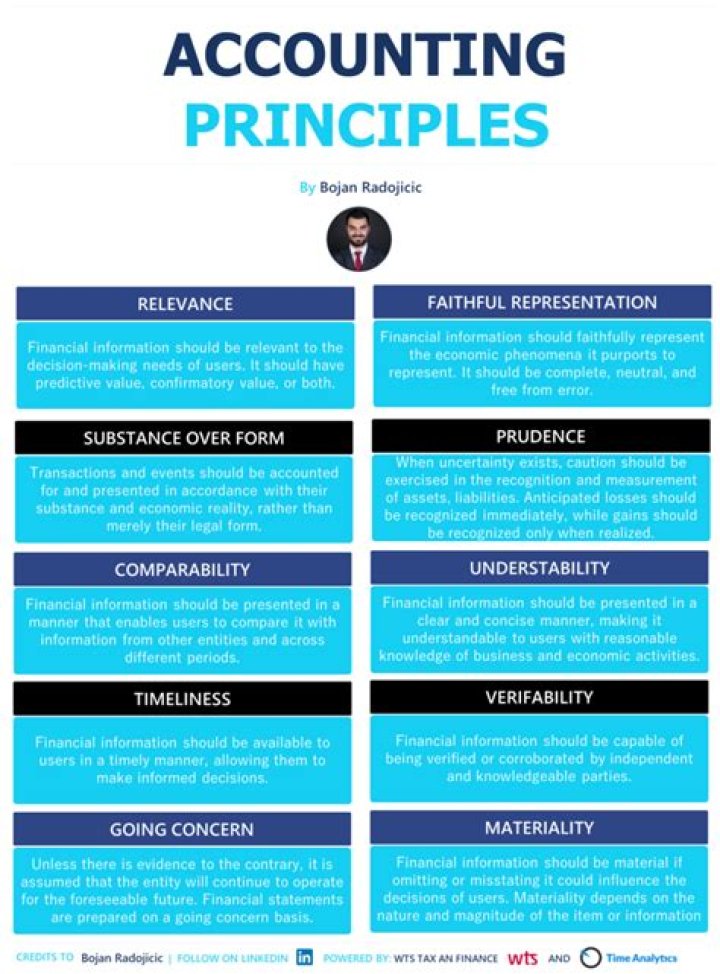

What are the 3 basic accounting principles?

- Debit the receiver and credit the giver. …

- Debit what comes in and credit what goes out. …

- Debit expenses and losses, credit income and gains.

Which accounting principle states that companies and owners should be treated as separate entities?

Answer: Business entity assumption, sometimes referred to as separate entity assumption or the economic entity concept, is an accounting principal that states that the financial records of any business must be kept separate from those of its owners or any other business.

What are the 10 principles of accounting?

- Economic Entity Principle. …

- Monetary Unit Principle. …

- Time Period Principle. …

- Cost Principle. …

- Full Disclosure Principle. …

- Going Concern Principle. …

- Matching Principle. …

- Revenue Recognition Principle.

What does the matching principle state?

In accrual accounting, the matching principle instructs that an expense should be reported in the same period in which the corresponding revenue is earned, and is associated with accrual accounting and the revenue recognition principle states that revenues should be recorded during the period in which they are earned, …

What is the realization principle and the matching principle?

While the realization principle determines when to record revenue during the selling and earning process, the matching principle considers the cost it took to make a sale and deducts this from the revenue made from the sale.

What is the matching principle in GAAP accounting?

The matching principle is part of the Generally Accepted Accounting Principles (GAAP), based on the cause-and-effect relationship between spending and earning. It requires that any business expenses incurred must be recorded in the same period as related revenues.