Why are interest only loans investment property

Nathan Sanders

Published Apr 13, 2026

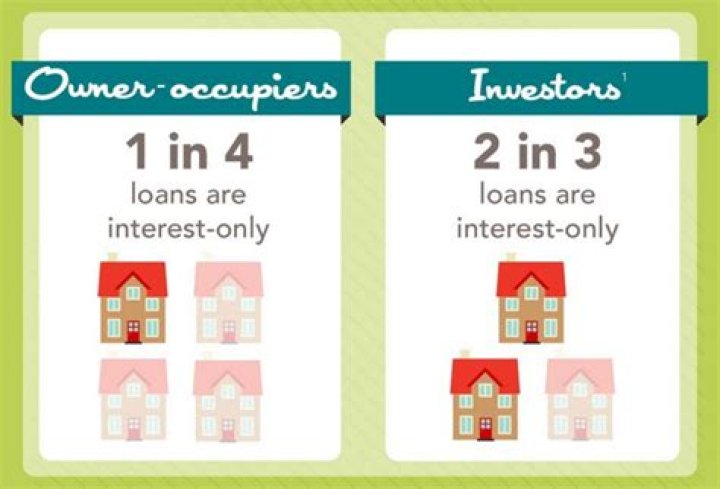

Interest-only investment loans are one way landlords are keeping costs down. Without the need to repay capital, the monthly payments are lower than for principal-plus-interest loans. This helps to maximise cash flow while continuing to benefit from capital growth.

Why do investors choose interest only loans?

Interest-only investment loans are one way landlords are keeping costs down. Without the need to repay capital, the monthly payments are lower than for principal-plus-interest loans. This helps to maximise cash flow while continuing to benefit from capital growth.

How long can you have an interest only loan on investment property?

While most banks only allow you to pay interest only for 5 years, there are others that allow interest only home loans for up to 15 years! Fix for up to 15 years. Switch back to principal and interest at any time. Make extra repayments with no limitations.

Can you get an interest only loan for an investment property?

Where an interest only loan used to purchase an investment property, the loan repayments only cover the interest, not the principal. In other words, the loan amount (principal) to purchase the property remains unpaid.Can you borrow more with an interest only loan?

Am I allowed to make extra repayments? Yes, banks usually allow you to make additional repayment on your loan. Making higher repayments can help you reduce the size of your loan much faster. It’s also an effective way to minimise the loan term and reduce the interest that you’ll pay.

What are the tax benefits of an investment property?

- Depreciation. Depreciation is the lowering in value of your property, as in the building itself, or the things within your property. …

- Negative Gearing. …

- Capital Gains Tax Exemptions. …

- Claiming Interest on Your Mortgage. …

- No Tax Paid on Withdrawals from Equity Loan.

Can you pay down the principal on an interest only loan?

You pay nothing off the principal during the interest-only period, so the amount borrowed doesn’t reduce. Your repayments will increase after the interest-only period, which may not be affordable.

What is better interest only or principal and interest?

By paying P&I, you’re paying off the mortgage earlier in the term so you end up paying less in interest. … Reduced interest rates: Making principal and interest repayments makes you a lower risk than a borrower making interest only repayments so banks are willing to offer you cheaper interest rates.Which is better paying principal or interest?

1. Save on interest. Since your interest is calculated on your remaining loan balance, making additional principal payments every month will significantly reduce your interest payments over the life of the loan. … Paying down more principal increases the amount of equity and saves on interest before the reset period.

Can you change from principal and interest to interest-only?You can change between principal and interest repayments and interest-only repayments to estimate the different interest charges.

Article first time published onWhat are the disadvantages of an interest-only mortgage?

- No Equity Growth. Interest-only mortgages today generally require large down payments so lenders have collateral against default. …

- Home Values are Falling. …

- Riskier loans with Higher Interest Rates. …

- Variable Interest Increases.

What happens when interest-only mortgage comes to an end?

When an interest-only mortgage ends, you have to repay all the amount you borrowed. The money to repay it can come from three sources: savings or investments; by getting a new mortgage; or.

How do you avoid taxes on investment property?

Investors can defer taxes by selling an investment property and using the equity to purchase another property in what is known as a 1031 like-kind exchange. Property owners can borrow against the home equity in their current property to make other investments.

Is buying an investment property a tax write off?

But if you borrow money to buy or improve an investment property, you can still deduct all the interest you pay on the loan. … Interest is deductible up to the total income you earn from the property in any given tax year, less any expenses you claim as miscellaneous itemized deductions.

How do I pay less taxes on investment property?

- Keep clear, up-to-date records of all your expenses.

- Understand the difference between capital works, repairs and maintenance.

- Claim capital assets and borrowing expenses.

- Track your depreciation and capital works schedule.

- Negatively gear your investment property.

Do extra payments automatically go to principal?

The interest is what you pay to borrow that money. If you make an extra payment, it may go toward any fees and interest first. … But if you designate an additional payment toward the loan as a principal-only payment, that money goes directly toward your principal — assuming the lender accepts principal-only payments.

What happens if I pay an extra $1000 a month on my mortgage?

Paying an extra $1,000 per month would save a homeowner a staggering $320,000 in interest and nearly cut the mortgage term in half. To be more precise, it’d shave nearly 12 and a half years off the loan term. The result is a home that is free and clear much faster, and tremendous savings that can rarely be beat.

How do I pay off a 30 year mortgage in 15 years?

- Adding a set amount each month to the payment.

- Making one extra monthly payment each year.

- Changing the loan from 30 years to 15 years.

- Making the loan a bi-weekly loan, meaning payments are made every two weeks instead of monthly.

How long can you have interest only loan?

So what is an interest-only home loan? Simply put, borrowers only have to pay the interest for the period as well as any fees for a fixed period of time, usually five to 10 years.

Can you switch from interest-only mortgage to repayment?

Yes, this is possible, as long as your mortgage lender approves you for a repayment mortgage. Switching to a repayment mortgage from an interest-only mortgage can be a good option for many borrowers and there are plenty of lenders who allow this.

Can I sell my house if I have an interest-only mortgage?

Sell the property You can of course sell a property to repay an interest-only mortgage. This is more common among those who buy to let. If you are lucky, the property price will cover the whole loan amount with some left over – but if you are unlucky and run into negative equity, you may have to cover a shortfall.

What is the point of interest-only mortgage?

An interest-only mortgage allows you to pay just the interest charged each month for the term of the loan. You don’t have to repay the amount you’ve borrowed until the end of the term.

Is it easier to get an interest-only mortgage?

Consider part repayment and part interest-only Those who have a repayment shortfall and are unable to borrow the full amount they need on interest-only can, with many mortgage lenders, split the loan – taking some on interest-only and the rest on repayment. This can make interest-only mortgages easier to get.

What is the 2 out of 5 year rule?

The 2-out-of-five-year rule is a rule that states that you must have lived in your home for a minimum of two out of the last five years before the date of sale. … You can exclude this amount each time you sell your home, but you can only claim this exclusion once every two years.

How does the IRS know if you have rental income?

An audit can be triggered through random selection, computer screening, and related taxpayers. Once you are selected for a tax audit, you will be contacted via mail to start the process of reviewing your records. At that point, the IRS will determine if you have any unreported rental income floating around.

How long do I have to live in my rental property to avoid capital gains?

If you like your rental property enough to live in it, you could convert it to a primary residence to avoid capital gains tax. There are some rules, however, that the IRS enforces. You have to own the home for at least five years. And you have to live in it for at least two out of five years before you sell it.

Can you claim mortgage interest on rental property?

Landlords are no longer able to deduct mortgage interest from rental income to reduce the tax they pay. You’ll now receive a tax credit based on 20% of the interest element of your mortgage payments. This rule change could mean that you’ll pay a lot more in tax than you might have done before.

What can you write off when you sell an investment property?

For example, you can deduct mortgage interest, property taxes, depreciation, insurance, repairs, maintenance, and other costs associated with operating the rental. And when it’s time to sell, you could end up with a tidy profit, especially if you’re in a hot real estate market.

What are the tax implications of owning a rental property?

If you own a property and rent it to tenants, how is that rental income taxed? The short answer is that rental income is taxed as ordinary income. If you’re in the 22% marginal tax bracket and have $5,000 in rental income to report, you’ll pay $1,100.