Why do lenders use FICO scores

Isabella Wilson

Published Apr 06, 2026

FICO Scores help lenders quickly, consistently and objectively evaluate potential borrowers’ credit risk. So when you apply for credit or a loan, there’s a very good chance your lender will use your FICO Scores to help them decide whether to approve you, and what terms and rates you qualify for.

What is a FICO score and why do lenders use it?

A FICO Score is a three-digit number based on the information in your credit reports. It helps lenders determine how likely you are to repay a loan. This, in turn, affects how much you can borrow, how many months you have to repay, and how much it will cost (the interest rate).

Why is your FICO score really important when applying for a loan?

Base scores show lenders the likelihood you’ll repay any credit obligation, whether it’s a credit card bill or loan payment. Industry-specific scores represent the odds you’ll repay a specific loan, such as an auto loan or mortgage.

Do most lenders use FICO scores?

FICO ® Scores are the most widely used credit scores—90% of top lenders use FICO ® Scores. Every year, lenders access billions of FICO ® Scores to help them understand people’s credit risk and make better–informed lending decisions.Is FICO more important than credit score?

“For years, there has been a lot of confusion among consumers over which credit scores matter. While there are many types of credit scores, FICO Scores matter the most because the majority of lenders use these scores to decide whether to approve loan applicants and at what interest rates.”

What FICO score do mortgage lenders use 2020?

The commonly used FICO® Scores for mortgage lending are: FICO® Score 2, or Experian/Fair Isaac Risk Model v2. FICO® Score 5, or Equifax Beacon 5. FICO® Score 4, or TransUnion FICO® Risk Score 04.

Is a FICO score of 8 GOOD OR BAD?

FICO 8 scores range between 300 and 850. A FICO score of at least 700 is considered a good score. There are also industry-specific versions of credit scores that businesses use. For example, the FICO Bankcard Score 8 is the most widely used score when you apply for a new credit card or a credit-limit increase.

What credit score is needed to buy a house 2020?

Generally speaking, you’ll need a credit score of at least 620 in order to secure a loan to buy a house. That’s the minimum credit score requirement most lenders have for a conventional loan.What credit score do FHA lenders use?

For those interested in applying for an FHA loan, applicants are now required to have a minimum FICO score of 580 to qualify for the low down payment advantage, which is currently at around 3.5 percent. If your credit score is below 580, however, you aren’t necessarily excluded from FHA loan eligibility.

How far back do mortgage Lenders look at credit history?The typical timeframe is the last six years. There are many factors that lenders consider when looking at your credit history, and each one is different. The typical timeframe is the last six years, but there are many different factors that lenders look at when reviewing your mortgage application.

Article first time published onIs FICO the same as Experian?

FICO® does this using complex algorithms based on information in your credit report from each of the national credit bureaus: Experian, TransUnion and Equifax. … FICO® also creates other types of scores that are based in part, or entirely, on your credit reports.

DO FICO scores matter?

If you want to borrow money to buy a car or a home, your FICO score matters – a lot. It plays a role in whether you get approved, the amount of the loan you’re offered, and the interest rate you’ll pay. A solid FICO credit score is also typically needed to qualify for a credit card.

Why is my FICO score so low?

Maxing out credit cards, paying late, and applying for new credit haphazardly are all things that lower FICO scores. More banks and lenders use FICO to make credit decisions than any other scoring or reporting model.

Why is Credit Karma so far off?

Credit Karma receives information from two of the top three credit reporting agencies. This indicates that Credit Karma is likely off by the number of points as the lack of information they have from Experian, the third provider that does not report to Credit Karma.

Does FICO use your credit history to determine your credit score?

Your credit score, also known as your FICO score, is used by lenders to determine your credit worthiness. Your score will go up or down based on your payment history, account balances, new inquiries and a number of other factors. For more information visit MyFICO.com.

What's a good FICO score?

Although ranges vary depending on the credit scoring model, generally credit scores from 580 to 669 are considered fair; 670 to 739 are considered good; 740 to 799 are considered very good; and 800 and up are considered excellent.

Can you get a home loan with 700 credit score?

A 700 credit score meets the minimum requirements for most mortgage lenders, so it’s possible to purchase a house when you’re in that range. … A credit score of 700 also might not qualify you for the best interest rate on your mortgage loan, you may still want to work on improving your credit scores to save on interest.

Do auto lenders use FICO score 8?

Most auto lenders use FICO Auto Score 8, as the most widespread, or FICO Auto Score 9. It’s the most recent and used by all three bureaus. FICO Auto Score ranges from 250 to 900, meaning your FICO score will differ from your FICO Auto Score.

Is a 900 credit score possible?

A credit score of 900 is either not possible or not very relevant. … On the standard 300-850 range used by FICO and VantageScore, a credit score of 800+ is considered “perfect.” That’s because higher scores won’t really save you any money.

How can I raise my mortgage FICO score?

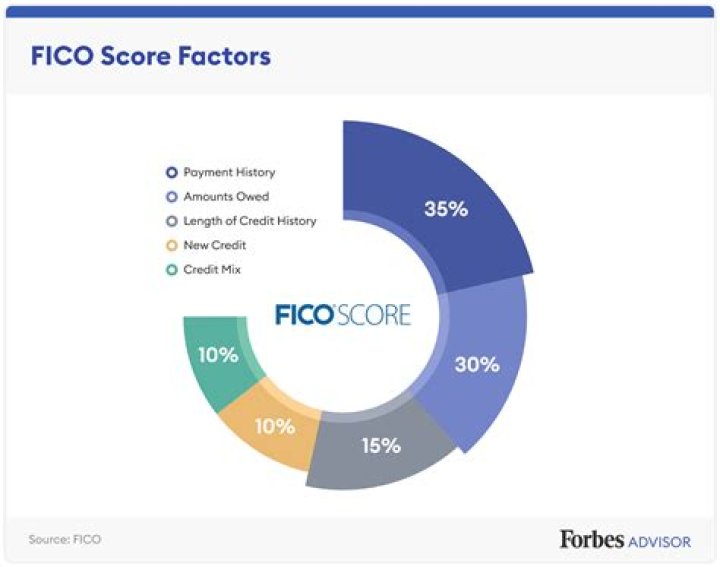

- Verify your accounts are current. “Payment History” makes the largest impact on your FICO score at 35 percent of your overall score. …

- Dispute your inaccuracies. …

- Ask for a little grace. …

- Settle up collections, charge–offs, judgments and liens. …

- Improve your debt utilization ratio.

Do mortgage lenders use middle score?

Lenders use these scores to calculate your risk of defaulting on a mortgage loan. Since each agency may report a slightly different score, lenders take the middle score of the three. For example, if your scores are 680, 710 and 660, lenders will use the middle score of 680 to assess your loan eligibility.

What credit score is needed to buy a home with low interest?

For most loan types, the credit score needed to buy a house is at least 620. But higher is better, and borrowers with scores of 740 or more will get the lowest interest rates.

How much do you need to make to qualify for a 200k mortgage?

A $200k mortgage with a 4.5% interest rate over 30 years and a $10k down-payment will require an annual income of $54,729 to qualify for the loan. You can calculate for even more variations in these parameters with our Mortgage Required Income Calculator.

What does my credit score need to be to buy a car?

What Is the Minimum Score Needed to Buy a Car? In general, lenders look for borrowers in the prime range or better, so you will need a score of 661 or higher to qualify for most conventional car loans.

How hard is it to get a FHA loan?

Read our editorial standards. To qualify for an FHA loan, you need a 3.5% down payment, 580 credit score, and 43% DTI ratio. An FHA loan is easier to get than a conventional mortgage. The FHA offers several types of home loans, including loans for home improvements.

What credit bureau is used to buy a house?

While the FICO® 8 model is the most widely used scoring model for general lending decisions, banks use the following FICO scores when you apply for a mortgage: FICO® Score 2 (Experian) FICO® Score 5 (Equifax) FICO® Score 4 (TransUnion)

How can I fix my credit quickly to buy a house?

- Reduce your credit card balances.

- Have friends or relatives with great credit add you to their accounts as an authorized user.

- Erase credit report errors with a rapid re–scorer (available only through your mortgage lender)

What is the average credit score by age?

AgeAverage FICO Score20-2966230-3967340-4968450-59706

Why would a mortgage be declined?

These are some of the common reasons for being refused a mortgage: You’ve missed or made late payments recently. You’ve had a default or a CCJ in the past six years. You’ve made too many credit applications in a short space of time in the past six months, resulting in multiple hard searches being recorded on your …

Why would an underwriter deny a loan?

Underwriters can deny your loan application for several reasons, from minor to major. … Some of these problems that might arise and have your underwriting denied are insufficient cash reserves, a low credit score, or high debt ratios.

What do lenders check right before closing?

Lenders want to know details such as your credit score, social security number, marital status, history of your residence, employment and income, account balances, debt payments and balances, confirmation of any foreclosures or bankruptcies in the last seven years and sourcing of a down payment.