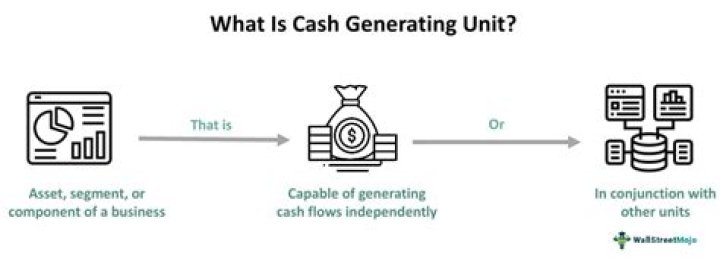

What is a CGU

Nathan Sanders

Published Mar 14, 2026

A Cash Generating Unit (CGU) is defined as the smallest identifiable group of assets that are able to generate cash inflows. … Identifying the different CGUs and their cash flows will enable us to test for impairment. Examples of CGUs include: an individual factory, a shop (from a chain of stores), etc…

What is an example of a CGU?

A Cash Generating Unit (CGU) is defined as the smallest identifiable group of assets that are able to generate cash inflows. … Identifying the different CGUs and their cash flows will enable us to test for impairment. Examples of CGUs include: an individual factory, a shop (from a chain of stores), etc…

What is the meaning of CGU?

A cash-generating unit is the smallest group of assets that independently generates cash flow and whose cash flow is largely independent of the cash flows generated by other assets. The concept is used by the international financial reporting standards in the determination of asset impairment.

How do you identify a CGU?

CGUs are identified at the lowest level to minimise the possibility that impairments of one asset or group will be masked by a high-performing asset. To identify a CGU, an entity asks two questions: Does a group of assets generate largely independent cash inflows? Is there an active market for the output?What is a CGU in accounting?

A cash-generating unit is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or groups of assets. … The recoverable amount of a CGU is the same as for an individual asset.

What is impairment loss investment?

The technical definition of the impairment loss is a decrease in net carrying value, the acquisition cost minus depreciation, of an asset that is greater than the future undisclosed cash flow of the same asset.

What is cash generating quizlet?

CASH GENERATING UNIT. THE SMALLEST IDENTIFIABLE GROUP OF ASSETS THAT GENERATE CASH INFLOWS FROM CONTINUING USE THAT ARE LARGELY INDEPENDENT OF THE CASH INFLOWS FROM OTHER ASSETS OR GROUP OF ASSETS.

Is investment in subsidiary a CGU?

Investment in subsidiaries in separate financial statements as a part of a larger CGU. … Additionally, it owns other individual non-financial assets directly. In consolidated financial statements of A, there is only one CGU consisting of assets held directly by A and its subsidiaries.How do you record an impairment reversal?

If the asset was not being carried at a revalued amount, then the gain on impairment would be recorded as a Gain in Impairment Reversal, directly in the Profit/Loss section of the Income Statement. If the asset was being carried at a revalued amount, we reverse the journal entry, based on the rules listed below.

Which assets can be impaired?Assets that are most likely to become impaired include accounts receivable, as well as long-term assets such as intangibles and fixed assets. When an impaired asset’s value is written down on the balance sheet, there is also a loss recorded on the income statement.

Article first time published onWhich assets are required to be tested for impairment annually?

The recoverable amount of the following assets in the scope of IAS 36 must be assessed each year: intangible assets with indefinite useful lives; intangible assets not yet available for use; and goodwill acquired in a business combination.

What are biological assets and bearer plants?

Biological assetA living animal or plantBearer plant*A living plant that: is used in the production or supply of agricultural produce is expected to bear produce for more than one period, and has a remote likelihood of being sold as agricultural produce, except for incidental scrap sales.

How is goodwill allocated to CGU?

Allocation of goodwill For impairment testing, goodwill is allocated (IAS 36.80-87) to the CGU that benefits from the synergies of the related business combination. If goodwill cannot be allocated on a non-arbitrary basis to individual CGUs, it is allocated to groups of CGUs.

What is a operating segment?

An operating segment is a component of an entity: [IFRS 8.2] that engages in business activities from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity)

How often should a cash-generating unit to which goodwill has been assigned be tested for impairment?

The goodwill of a reporting unit should be tested for impairment on an annual basis, which can be performed at the same time in each succeeding year. It is not necessary to test all reporting units at the same time.

Is money which is coming into the business?

Cash incoming – money that is flowing into the business. Cash outgoing – money that is flowing out of the business.

When a note receivable is determined to be impaired?

A loan is considered to be impaired when it is probable that not all of the related principal and interest payments will be collected.

Can impairment loss be reversed?

An impairment loss may only be reversed if there has been a change in the estimates used to determine the asset’s recoverable amount since the last impairment loss had been recognised. If this is the case, then the carrying amount of the asset shall be increased to its recoverable amount.

What is the accounting for goodwill?

Goodwill is an intangible asset that accounts for the excess purchase price of another company. … Goodwill is calculated by taking the purchase price of a company and subtracting the difference between the fair market value of the assets and liabilities.

Does impairment affect net income?

An impairment loss makes it into the “total operating expenses” section of an income statement and, thus, decreases corporate net income.

Is impairment loss a debit or credit?

A loss on impairment is recognized as a debit to Loss on Impairment (the difference between the new fair market value and current book value of the asset) and a credit to the asset. The loss will reduce income in the income statement and reduce total assets on the balance sheet.

Can a brand be Capitalised?

Brand, because it is an intangible asset, is similar to a machine. But, unfortunately, generally accepted accounting principles (GAAP) allow finance professionals to only capitalize some brand expenses and not others.

Why do entities acquire property plant and equipment?

Such items of property, plant, and equipment qualify for recognition as assets, because they enable an entity to derive future economic benefits or service potential from related assets in excess of what could be derived had those items not been acquired.

What is a cash generating unit CGU in IFRS give an example?

A cash-generating unit is an identifiable assets group provides money inflows to a company, these cash flows are independent of those generated by other types of assets. For example, a company has 50 hotels worldwide.

When goodwill Cannot be allocated to CGU which test is performed?

Thus, when all or a portion of goodwill cannot be allocated reasonably and consistently to the CGU being tested for impairment, two levels of impairment tests are carried out, viz., bottom-up test and top-down test.

When a cash generating unit has an impairment loss the loss must first be applied to?

section 8 explains that any impairment loss must be allocated to the assets in the CGU in a specific order: i) first against any goodwill allocated to the CGU; ii) then against the other assets of the CGU on a pro rata basis.

Which of the following assets is are known as active assets?

An active asset is an asset that is used by a business in its daily or routine business operations. Active assets can be tangible–such as buildings or equipment–or intangible–such as patents or copyrights.

How do you tell if an asset is impaired?

An impaired asset is an asset valued at less than book value or net carrying value. In other words, an impaired asset has a current market value that is less than the value listed on the balance sheet. To account for the loss, the company’s balance sheet must be updated to reflect the asset’s new diminished value.

Which of the following is not an investment property?

Examples of assets that are not investment property are property intended for sale in the near term, property being constructed for a third party, owner-occupied property, and property leased to a third party under a finance lease.

What is the difference between impairment and write off?

In accounting, impairment is a permanent reduction in the value of a company asset. … If the book value of the asset exceeds the future cash flow or other benefit of the asset, the difference between the two is written off, and the value of the asset declines on the company’s balance sheet.

Where does impairment go on the income statement?

Impairment is a non-cash expense that is reported under the operating expenses section of the income statement.