What counts as a qualified retirement plan

Isabella Wilson

Published Mar 12, 2026

A qualified retirement plan is a retirement plan recognized by the IRS where investment income accumulates tax-deferred. Common examples include individual retirement accounts (IRAs), pension plans and Keogh plans. Most retirement plans offered through your job are qualified plans.

What is considered a qualified retirement plan?

A qualified retirement plan is a retirement plan established by an employer that is designed to provide retirement income to designated employees and their beneficiaries, which meets certain IRS Code requirements in terms of both form and operation.

What makes a qualified plan qualified?

Answer: A qualified plan is an employer-sponsored retirement plan that qualifies for special tax treatment under Section 401(a) of the Internal Revenue Code. … That is, you don’t pay income tax on amounts contributed by your employer until you withdraw money from the plan.

Does a 401k count as a qualified retirement plan?

Yes, a 401(k) is usually a qualified retirement account. Defined-benefit and defined-contribution plans are two of the most popular categories of qualified plans.How do I know if my pension is a qualified plan?

A retirement or pension fund is “qualified” if it meets the federal standards promulgated by the Employee Retirement Income Security (ERISA).

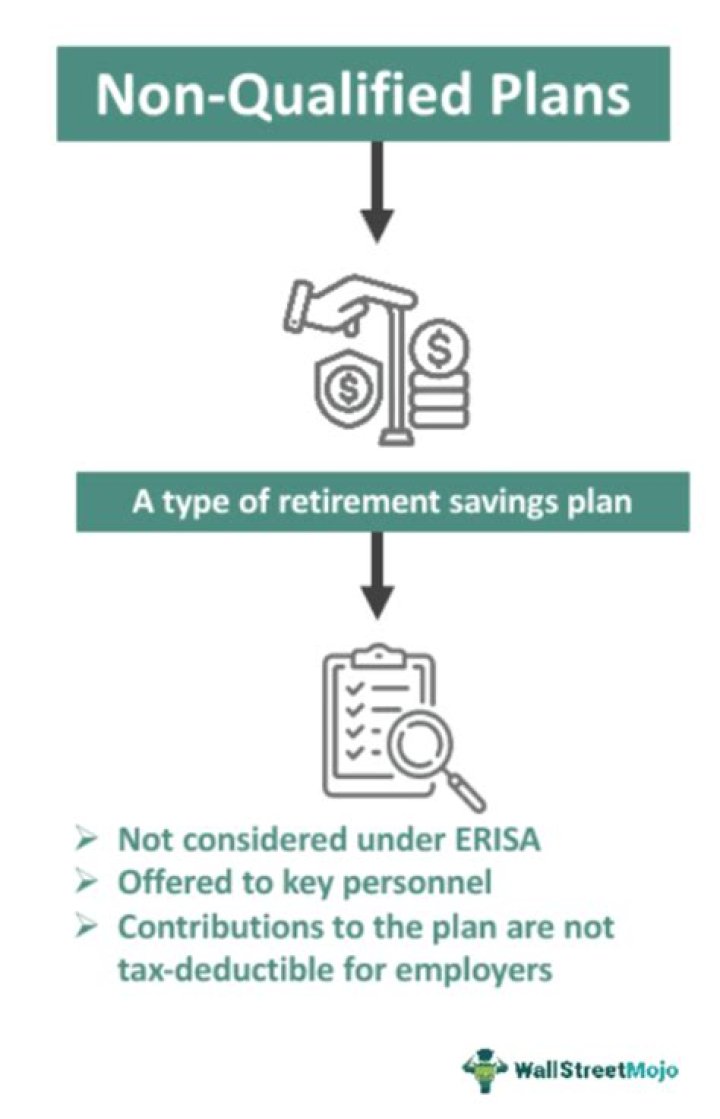

What are non qualified retirement plans?

A nonqualified retirement plan is one that’s not subject to the Employee Retirement Income Security Act of 1974 (ERISA). Most nonqualified plans are deferred compensation arrangements, or an agreement by an employer to pay an employee in the future.

Is a 403 B a qualified retirement plan?

401(k) and 403(b) plans are qualified tax-advantaged retirement plans offered by employers to their employees. 401(k) plans are offered by for-profit companies to eligible employees who contribute pre or post-tax money through payroll deduction.

Is an IRA considered a qualified retirement plan?

A qualified retirement plan is a retirement plan recognized by the IRS where investment income accumulates tax-deferred. Common examples include individual retirement accounts (IRAs), pension plans and Keogh plans. Most retirement plans offered through your job are qualified plans.Are IRAs qualified or nonqualified?

What Is a Qualified Retirement Plan? Qualified retirement plans are designed to meet ERISA guidelines and, as such, qualify for tax benefits on top of those received by regular retirement plans, such as IRAs.

Is a Roth IRA considered a qualified retirement plan?Qualified retirement plans are recognized by the IRS and meet requirements laid out in Section 401(a) of the U.S. tax code and ERISA guidelines. … A Roth IRA is not a qualified retirement plan, but there are similar tax advantages for those planning for retirement.

Article first time published onWhat type of accounts are non-qualified?

The type of investments that can be held in non-qualified accounts are annuities, mutual funds, equities, etc. If non-qualified accounts are invested in annuities, the growth on those accounts would grow on a tax deferred basis and the earnings are taxable at the time of withdrawal.

Can I open a 403 B on my own?

You cannot open your own 403(b) plan because that is an employer funded account only. However, depending on the plan administrator’s policy at work, it may be possible to have more income sent to your 403b designated as a 2017 contribution if allowed. But you cannot open up a new account on your own.

Is 403b pretax or post tax?

Because 403(b) contributions are made pretax, you must pay taxes on the withdrawals you make in retirement. Distributions can begin without penalty at age 59½.

What is difference between 403b and 457b?

There are two different types of 457 plans—the 457(b), which is offered to state and local government employees, and the 457(f) is for top executives in nonprofits. A 403(b) plan is typically offered to employees of private nonprofits and government workers, including public school employees.

What are non-qualified assets?

Non-Qualified Savings The term “non-qualified” refers to any asset that is not part of a qualified plan. For example, your bank account is a non-qualified asset. You may also have an investment account outside of your retirement plan. That is also considered to be “non-qualified”.

How are IRAs similar to qualified plans?

IRAs and qualified plans are similar in several ways but have one noteworthy difference: An IRA is a retirement account for one person, while qualified retirement plans are owned and administered by employers. With both, the onus is on you, not your employer, to plan for your retirement savings needs.

What retirement plans do not qualify for federal income tax deduction?

Description:Roth IRAs are a special type of Individual Retirement Account. If you qualify for a Roth plan, you can contribute funds up to a certain amount, but contributions are taxed as income. You cannot deduct the contributions.

What are the two general categories of qualified retirement plans?

Qualified retirement plans are grouped into two primary categories: defined benefit plans and defined contribution plans.

Are individual accounts qualified?

Individual Qualified Accounts can be opened at a Brokerage firm, bank, or credit union. Like Nonqualified Accounts, you use after-tax dollars to contribute.

Is a Roth IRA a qualified asset?

The Bottom Line. A qualified retirement plan is a retirement plan that is only offered by an employer and that qualifies for tax breaks. By its definition, an IRA is not a qualified retirement plan as it is not offered by employers, unlike 401(k)s, which are, making them qualified retirement plans.

What is the difference between a qualified and nonqualified dividend?

There are two types of ordinary dividends: qualified and nonqualified. The most significant difference between the two is that nonqualified dividends are taxed at ordinary income rates, while qualified dividends receive more favorable tax treatment by being taxed at capital gains rates.

What are the disadvantages of a 403 B?

ProsConsTax advantagesFew investment choicesHigh contribution limitsHigh feesEmployer matchingPenalties on early withdrawalsShorter vesting schedulesNot always subject to ERISA

Can you lose money in a 403 B?

Your contributions to your 403(b) can’t be taken away or forfeited. Contributions to your 403(b) made by your employer may be subject to vesting requirements. In this case, any money that isn’t vested as of the date you were fired or laid off is no longer yours.

Is a 403b better than a 401k?

Because 401(k) plans are more expensive for the company, they usually offer a wider range and sometimes better quality of investment options. Employer Match: Both plans allow for employer matching, but fewer employers offer matches with their 403(b) plans. … 401(k) plans are more expensive for employers.

Are 403 B contributions Pretax?

One important feature of a 403(b) plan is your ability to make pretax contributions to the plan. Pretax means that your contributions are deducted from your pay and transferred to the 403(b) plan before federal (and most state) income taxes are calculated.

Are 401k pre-tax?

Contributions to tax-advantaged retirement accounts, such as a 401(k), are made with pre-tax dollars. That means the money goes into your retirement account before it gets taxed. … That means you don’t owe any income tax until you withdraw from your account, typically after you retire.

Is Roth 403b pre-tax?

An additional way to save in your plan Unlike a traditional pretax 403(b), the Roth 403(b) allows you to contribute after-tax dollars and then withdraw tax-free dollars from your account when you retire.

Is a 457b a qualified retirement plan?

A 457(b) plan is a non-qualified deferred compensation plan available to certain government employees (including state and local workers, police officers, firefighters, and some teachers), as well as highly compensated employees of non-profit organizations.

Can I have both 403b and 457b?

Tax law allows you to contribute to both 403(b) and 457(b) plans (governmental or non-governmental), and not have contributions to one offset the other. You can “max out” both plans by contributing up to $20,500 to each in 2022, giving you the opportunity to defer up to $41,000 annually on a pre-tax basis.

What is a 457b retirement plan?

A 457(b) plan is an employer-sponsored, tax-favored retirement savings account. With this type of plan, you contribute pre-tax dollars from your paycheck, and that money won’t be taxed until you withdraw the money, usually for retirement.