What is a large accelerated filer

Rachel Hunter

Published Apr 10, 2026

A large accelerated filer must have an aggregate worldwide public float of $700 million or more, as of the last business day of its most recently completed second fiscal quarter, and also satisfy the second and third conditions above.

How many days does a large accelerated filer have to file 10k?

10-Q and 10-K Filing DeadlinesCompany Category10-Q Deadline10-K DeadlineLarge Accelerated Filer ($700MM or more)40 days60 daysAccelerated Filer ($75–$700MM)40 days75 daysNon-accelerated Filer (less than $75MM)45 days90 days

Is a smaller reporting company a non-accelerated filer?

It will be a non-accelerated filer if it has less than $100 million in revenues. If its revenues are $100 million or more, it will be an accelerated filer.

Who is a non-accelerated filer?

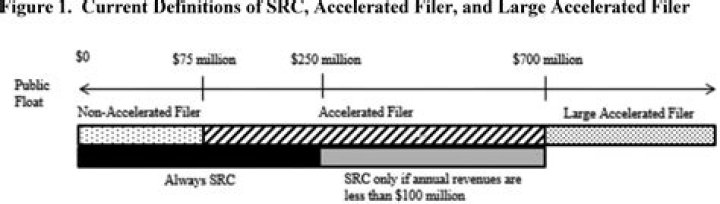

Non-Accelerated Filer – a public float of less than $75 million, qualifies as an SRC under the SRC revenue test referenced below or does not otherwise meet the requirements of a large accelerated filer or an accelerated filer.Which threshold is not a requirement to meet the definition of a large accelerated filer as defined in Rule 12b-2 of the Exchange Act?

Rule 12b-2 defines a “large accelerated filer” in the same manner except that the issuer’s public float must be $700 million or more.

What does it mean to be an accelerated filer?

As discussed above, in order to be categorized as an accelerated filer, an issuer must have a public float of $75 million or more, but less than $700 million, as of the last business day of its most recently completed second fiscal quarter. A large accelerated filer must have a public float greater than $700 million.

How do I know if my accelerated filer is large?

A large accelerated filer must have an aggregate worldwide public float of $700 million or more, as of the last business day of its most recently completed second fiscal quarter, and also satisfy the second and third conditions above.

What is a domestic filer?

SEC Expert: Domestic Filers is an end-to-end compliance solution for US corporations filing with the SEC, and the accountants, auditors, and attorneys who advise them. … Completing periodic, registration, and other SEC filings in a timely, accurate manner.Can an emerging growth company be an accelerated filer?

An emerging growth company (EGC) is any company that meets the following requirements: … the company cannot have issued more than $1 billion in non-convertible bonds within the last 3 years, and. the company does not qualify as a large accelerated filer, meaning a public float of over $700 million.

What is an emerging growth company SEC?A company qualifies as an emerging growth company if it has total annual gross revenues of less than $1.07 billion during its most recently completed fiscal year and, as of December 8, 2011, had not sold common equity securities under a registration statement. …

Article first time published onCan you be a large accelerated filer and smaller reporting company?

A registrant may qualify as a smaller reporting company at the same time it may also qualify as an accelerated filer, large accelerated filer, or non-accelerated filer.

What is considered a smaller reporting company?

An entity is a smaller reporting company if it has annual revenues of less than $100 million and either (1) no public float (because it has no public equity outstanding or no public trading market for its equity exists) or (2) a public float of less than $700 million.

Can you be an emerging growth company and a smaller reporting company?

Regulation S-KItemScaled Disclosure AccommodationRuleScaled Disclosure

What is Section 13 or 15 D of the Securities Exchange Act of 1934?

Also known as US reporting company or US public company. A company subject to Section 13 or 15(d) of the US Securities Exchange Act of 1934 (Exchange Act), which requires the company to file periodic reports with the US Securities and Exchange Commission (SEC).

When must a LAF foreign company file its annual report?

A foreign private issuer must file its annual report on Form 20-F within six months after the end of the fiscal year covered by the report.

Who does Regulation SK apply to?

They are required to file Form S-1 as the registration statement this is the first time the Regulation S-K applies to a company. After that, they need to fulfill the ongoing filing requirements using forms 10-K and 8-K. This regulation helps the investors to make informed decisions while investing in a company.

How do I check my SEC file status?

A company’s status can be determined by using public float and annual revenue numbers to work from left to right across a row in Table 1. For example, a company with a public float of $215 million and $110 million in annual revenue would fall into the third row of Table 1, qualifying as an SRC and accelerated filer.

What did the Securities Exchange Act of 1934 do?

Securities Exchange Act of 1934. With this Act, Congress created the Securities and Exchange Commission. The Act empowers the SEC with broad authority over all aspects of the securities industry. … The Act also empowers the SEC to require periodic reporting of information by companies with publicly traded securities.

How do you calculate global aggregate market value?

Aggregate worldwide market value is calculated by multiplying the aggregate number of shares of voting and non-voting common equity the registrant has outstanding by the price at which such common equity was last sold, or the average of the bid and asked prices of such common equity, in the principal market for such …

What is an accelerated filer?

Under the previous definition, an issuer with public float of $75 million or greater qualified as an accelerated filer. … Under the amended rule, other than during a transition period, issuers with public float between $75 and $700 million and $100 million or more in annual revenue qualify as an accelerated filer.

What does it mean to be a non-accelerated filer?

A reporting company that does not meet the requirements to be an accelerated filer or a large accelerated filer (see Rule 12b-2 under the Exchange Act). A non-accelerated filer has a public float of less than $75 million.

What is a non-accelerated filer?

A non-Accelerated Filer is a Reporting Company that, as a result of having a public float of less than $75 million, has not had to accelerate its periodic reporting deadlines.

Can an EGC be a large accelerated filer?

Once non-affiliated public float exceeds $700 million, you will soon trigger large accelerated filer status, exit EGC, and be subject to ICFR attestation requirements.

Can you be an EGC and SRC?

A company may qualify as both an SRC and an emerging growth company (EGC);4 however, unlike the scaled disclosures available for an EGC, there is no time limit for qualifying as an SRC.

Can a private company be an emerging growth company?

A foreign private issuer qualifies as an emerging growth company and is also entitled to submit its draft registration statement on a non-public basis pursuant to the Division’s policy on Non-Public Submissions from Foreign Private Issuers.

What is a 10-K report?

A 10-K is a comprehensive report filed annually by public companies about their financial performance. … Information in the 10-K includes corporate history, financial statements, earnings per share, and any other relevant data. The 10-K is a useful tool for investors to make important decisions about their investments.

Where can I download 10-K reports?

But, you can get recent ones by going to , clicking EDGAR search options and then recent filings. On the recent filings page, there is an option to search by form type. Put in 10-K and it should produce all recent annual reports.

What does SEC EDGAR mean?

EDGAR, the Electronic Data Gathering, Analysis, and Retrieval system, is the primary system for companies and others submitting documents under the Securities Act of 1933, the Securities Exchange Act of 1934, the Trust Indenture Act of 1939, and the Investment Company Act of 1940.

What financial information may an emerging growth company omit from its draft and publicly filed registration statements?

Answer: Under Section 71003 of the FAST Act, an Emerging Growth Company may omit from its filed registration statements annual and interim financial information that “relates to a historical period that the issuer reasonably believes will not be required to be included…at the time of the contemplated offering.” Interim …

What happens when you lose EGC status?

A company that has lost EGC status does not need to present, in subsequently filed registration statements and periodic reports, selected financial data for periods prior to the earliest audited period presented in its initial Securities Act or Exchange Act registration statement.

Can a SPAC be an EGC?

A SPAC may be considered an emerging growth company (“EGC”) as defined in Section 2(a)(19) of the Securities Act, and if so it will remain an EGC until the earlier of (i) the last day of the fiscal year (a) Page 5 WHAT’S THE DEAL? SPACs | 5 following the fifth anniversary of the completion of the IPO, (b) in which the …